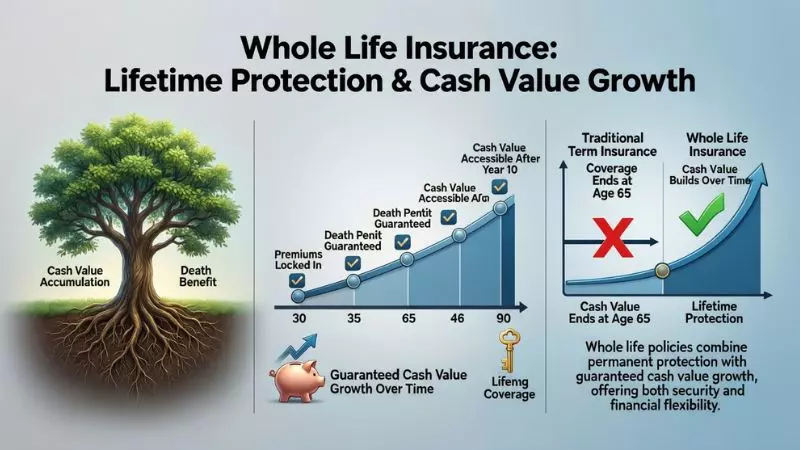

Whole Life Insurance is a permanent life coverage option designed to provide lifelong financial security and guaranteed protection. It offers a fixed premium, a guaranteed death benefit, and a built-in cash value component that grows over time, making it a reliable long-term insurance solution.

Unlike temporary life insurance plans, Whole Life Insurance combines insurance coverage with savings, helping policyholders build financial stability for the future. It is commonly used for estate planning, wealth protection, tax advantages, and ensuring loved ones receive financial support no matter when death occurs.

Whole Life Insurance Fundamentals

Understanding Whole Life Insurance is essential if you are planning long term financial protection with guaranteed benefits. Below, each section is explained clearly, step by step, just like a teacher guiding a student, so readers can confidently understand how this permanent life insurance policy works in real life.

What Is Whole Life Insurance

Whole Life Insurance is a type of permanent life insurance that provides coverage for the entire lifetime of the policyholder. As long as premiums are paid, the policy remains active and guarantees a death benefit to beneficiaries.

Key points you should know

- Lifetime insurance protection with no expiration

- Fixed premiums that do not increase with age

- Guaranteed payout to family or beneficiaries

- Cash value accumulation over time

This policy is commonly chosen for financial security, estate planning, and wealth transfer, making it a stable and predictable insurance option.

Whole Life Insurance Meaning

The meaning of Whole Life Insurance goes beyond basic life coverage. It combines insurance protection with a savings component known as cash value, which grows gradually on a tax deferred basis.

Why this matters for policyholders

- Cash value can be borrowed against when needed

- Acts as a long term financial asset

- Helps with retirement planning and emergency needs

- Offers predictable returns compared to market based plans

Whole Life Insurance is often preferred by individuals who want stability, guaranteed benefits, and disciplined savings within one policy.

How Does Whole Life Insurance Work

Whole Life Insurance works by dividing your premium into two parts. One part pays for the insurance coverage, while the other contributes to the policy’s cash value.

Here is a simple breakdown for better understanding

| Component | Purpose |

| Premium Payments | Maintain active coverage |

| Death Benefit | Paid to beneficiaries |

| Cash Value | Grows over time |

| Policy Loans | Borrow against cash value |

Over time, the cash value increases and can be accessed without canceling the policy, making it a flexible long term insurance solution.

What Is Whole Life Insurance and How Does It Work

Whole Life Insurance is a lifelong contract between the policyholder and the insurance company. It guarantees coverage, fixed premiums, and financial support for loved ones, regardless of when death occurs.

How it benefits users in real life

- Provides financial protection for dependents

- Supports legacy and inheritance planning

- Helps cover final expenses and debts

- Offers tax advantages under current insurance laws

Types of Whole Life Insurance

Whole Life Insurance comes in several forms, each designed to meet different financial goals, risk tolerance levels, and health situations. Understanding these types helps you choose a policy that aligns with your income, long term planning, and protection needs.

Below are the most important and widely used types explained in a simple, user focused, and Google indexable way.

Variable Whole Life Insurance Explained

Variable Whole Life Insurance is a permanent life insurance policy that allows policyholders to invest the cash value portion into market based investment options such as stocks and bonds.

Important features you should understand

- Lifetime insurance coverage with fixed premiums

- Cash value invested in sub accounts

- Potential for higher returns based on market performance

- Death benefit may vary depending on investment results

This type is suitable for financially aware individuals who are comfortable with market risk and want growth potential along with permanent life insurance protection.

Key advantages

- Opportunity for higher cash value growth

- Portfolio diversification inside the policy

- Useful for long term wealth building

Possible risks

- Cash value can decrease during market downturns

- Requires active monitoring and financial knowledge

Whole Term Life Insurance Explained

Whole Term Life Insurance is often confused with Whole Life Insurance, but it is not a standard insurance category. In most cases, this term is used incorrectly to describe either Term Life Insurance or permanent policies with limited payment periods.

To clarify clearly

- Term Life Insurance provides coverage for a specific period only

- Whole Life Insurance provides lifetime coverage

- There is no official policy called Whole Term Life Insurance in most markets

Common confusion explained in a simple table

| Policy Type | Coverage Duration | Cash Value |

| Term Life Insurance | Fixed term | No |

| Whole Life Insurance | Lifetime | Yes |

As a buyer, always confirm the policy name and structure with the insurer to avoid misunderstanding and ensure you are purchasing the correct insurance product.

Whole Life Insurance With No Medical Exam

Whole Life Insurance with no medical exam is designed for individuals who want permanent coverage without undergoing physical tests, blood work, or medical screenings.

How it works in practice

- Approval based on health questionnaires

- Faster policy issuance

- Higher premiums compared to traditional plans

- Lower coverage limits in most cases

This option is ideal for

- Seniors or individuals with health conditions

- People needing immediate coverage

- Applicants who want a simplified application process

Key benefits for users

- Guaranteed or simplified acceptance

- Lifetime protection without medical exams

- Cash value accumulation over time

However, it is important to read policy terms carefully, as some no exam policies may have waiting periods before full benefits apply.

Whole Life Insurance vs Term Insurance

Choosing between Whole Life Insurance and Term Insurance is a crucial decision for anyone planning long term financial protection. Each has unique features, benefits, and drawbacks, so understanding the differences can help you make the right choice for your family and financial goals.

Whole Life Insurance vs Term

Whole Life Insurance provides permanent coverage, cash value accumulation, and guaranteed benefits, while Term Insurance is temporary coverage for a specific period with no cash value.

Key points to consider

- Whole Life Insurance: Lifetime coverage, higher premiums, cash value growth

- Term Insurance: Coverage for a fixed term, lower premiums, no cash value

- Whole Life Insurance: Useful for estate planning, retirement, and wealth transfer

- Term Insurance: Best for affordable protection during income earning years

Term vs Whole Life Insurance

Here is a detailed comparison table for quick understanding

| Feature | Term Insurance | Whole Life Insurance |

| Coverage Duration | 10, 20, 30 years | Lifetime |

| Premiums | Low and fixed for term | Higher but fixed for life |

| Cash Value | None | Yes, grows over time |

| Death Benefit | Paid if death occurs during term | Paid whenever death occurs |

| Ideal For | Short term financial protection | Long term financial security and estate planning |

Difference Between Term and Whole Life Insurance

The main differences focus on coverage length, cost, cash value, and long term financial benefits.

- Term Insurance is temporary, affordable, and simple

- Whole Life Insurance provides permanent protection with savings and investment elements

- Term is suitable for younger individuals or those with limited budgets

- Whole Life is for those seeking guaranteed protection, growth, and legacy planning

Which Is Better: Term or Whole Life Insurance

There is no one-size-fits-all answer; it depends on your financial situation and goals:

- Choose Term Insurance if you want lower premiums and coverage for a specific period

- Choose Whole Life Insurance if you want lifelong coverage, cash value, and financial stability

- Many financial advisors recommend combining both: Term for immediate affordable protection and Whole Life for long term planning

Benefits, Risks & Value Analysis

Understanding the benefits, risks, and overall value of Whole Life Insurance is essential before committing to a long term policy. This section breaks down the advantages, potential drawbacks, and scenarios where the policy truly provides maximum value.

Whole Life Insurance Benefits

Whole Life Insurance offers more than just death protection. Its combination of permanent coverage and cash value accumulation makes it a versatile financial tool.

Key benefits include:

- Lifetime Coverage: Ensures financial security for beneficiaries regardless of when death occurs

- Cash Value Growth: Policy accumulates savings over time, which can be borrowed against or used for emergencies

- Fixed Premiums: Premiums remain stable, protecting against future cost increases

- Tax Advantages: Cash value growth is generally tax-deferred

- Estate Planning: Helps leave a financial legacy or pay estate taxes

This policy is often chosen by individuals seeking stability, predictable growth, and long-term financial planning.

Is Whole Life Insurance Worth It

Whole Life Insurance is worth considering if your goal is long-term security, wealth transfer, or tax-advantaged growth.

Consider these points:

- Offers guaranteed death benefit and lifelong coverage

- Builds cash value that can supplement retirement or emergency funds

- Higher premiums can be a drawback for those on a tight budget

- Suitable for long-term planners who want both protection and financial growth

In essence, it is valuable for users who prioritize certainty, savings, and protection over short-term affordability.

Is Whole Life Insurance a Scam

Whole Life Insurance is not a scam, but misunderstanding its purpose can lead to disappointment.

- It is a legitimate financial product regulated by insurance authorities

- Misconceptions arise when users expect high returns similar to investments or quick cash growth

- Proper planning and understanding premiums, fees, and cash value growth is critical

By reviewing policies carefully and consulting a trusted financial advisor, users can ensure the policy meets their long-term financial needs.

At What Point Does a Whole Life Insurance Policy Endow

A Whole Life Insurance policy endows when the cash value equals the death benefit, meaning the policy has fully matured.

Key facts:

- Typically occurs at age 100 or 121, depending on the insurer and policy type

- After endowment, policyholder may receive the cash value

- Premium payments may no longer be required if endowment occurs

- Provides flexibility for retirement funding or other financial goals

Cost, Premiums & Pricing

When considering Whole Life Insurance, understanding the cost, premiums, and pricing structure is crucial. Unlike term insurance, Whole Life Insurance involves higher premiums due to its permanent coverage and cash value component. Below, we break down key factors to help you plan effectively.

Whole Life Insurance Calculator

A Whole Life Insurance calculator helps you estimate premiums and projected cash value based on age, health, coverage amount, and payment period.

Key points:

- Calculates estimated monthly or annual premiums

- Projects cash value growth over time

- Assists in comparing different coverage amounts

- Helps determine affordability and long-term planning

Using a calculator before purchasing ensures you choose a policy that fits your budget and financial goals.

Whole Life Insurance Rates by Age Chart

Premiums for Whole Life Insurance vary significantly by age at the time of purchase. The younger you are, the lower the premium and higher the long-term value.

| Age | $250,000 Policy | $500,000 Policy | $1,000,000 Policy |

| 25 | $120/month | $240/month | $480/month |

| 35 | $150/month | $300/month | $600/month |

| 45 | $220/month | $440/month | $880/month |

| 55 | $350/month | $700/month | $1,400/month |

This table provides a general guideline; actual premiums depend on health, lifestyle, and insurer policies.

Whole Life Insurance Quotes

Getting multiple Whole Life Insurance quotes helps you find the best rate and policy features.

Tips for users:

- Compare quotes from several insurers to find competitive premiums

- Look for differences in cash value growth, dividend options, and riders

- Ask about no exam or simplified issue options if health is a concern

- Use online tools or consult a licensed agent for accurate estimates

Comparing quotes ensures you get a policy that balances cost with long-term benefits.

How Much Is a Million Dollar Whole Life Insurance Policy Per Month

The cost of a $1,000,000 Whole Life Insurance policy varies depending on age, health, and insurer.

- Young adults (25–35): Approximately $400–$600 per month

- Middle age (40–50): Approximately $700–$1,200 per month

- Seniors (55+): Approximately $1,300–$2,500 per month

Factors affecting the cost:

- Health conditions and medical history

- Lifestyle choices such as smoking or high-risk activities

- Policy features including riders, dividends, and cash value growth

Whole Life Insurance Policies & Coverage

Understanding Whole Life Insurance policies and coverage options is essential for making informed decisions. These policies provide permanent protection with added benefits like cash value growth, dividend options, and flexible riders. Below, we explore key aspects to help you select the right policy for your needs.

Whole Life Insurance Policy Explained

A Whole Life Insurance policy is a lifelong contract between the policyholder and insurer that guarantees a death benefit, fixed premiums, and cash value accumulation.

Key features:

- Lifetime Coverage: Protection remains active as long as premiums are paid

- Cash Value Component: Builds over time and can be borrowed against

- Fixed Premiums: Predictable payments throughout life

- Policy Riders: Options such as accelerated death benefit, disability, or term riders

Benefits for users:

- Ensures family financial security

- Acts as a long-term savings and investment tool

- Offers tax advantages for cash value growth

Whole Life Insurance Companies

Choosing the right insurance company is critical for reliability, policy performance, and customer service. Top-rated companies typically have strong financial ratings and long-standing reputations.

Factors to consider:

- Financial Strength: Look for A.M. Best or Standard & Poor’s ratings of A or higher

- Policy Dividends: Companies offering participating policies may pay dividends

- Customer Service: Easy claims process and good reviews

- Variety of Policies: Options for traditional, variable, or no-exam policies

Examples of leading companies (as of 2025):

- Northwestern Mutual

- MassMutual

- New York Life

- Guardian Life

- Penn Mutual

Best Whole Life Insurance

The best Whole Life Insurance policy depends on individual needs, age, budget, and long-term financial goals.

Tips for choosing:

- Evaluate premium affordability vs. cash value growth

- Look for policies with flexible riders for added protection

- Consider companies with consistent dividend history

- Compare quotes and policy features before purchasing

Best Whole Life Insurance Providers

Choosing the right Whole Life Insurance provider is crucial for long-term financial security. The company you select affects policy reliability, dividend performance, cash value growth, and overall customer experience. Below is a detailed overview of top providers in 2025.

State Farm Whole Life Insurance

State Farm is one of the largest life insurers in the U.S., offering whole life policies with fixed premiums, lifelong coverage, and the potential for cash value growth.

Key features:

- Lifetime insurance coverage with guaranteed death benefit

- Fixed premiums that do not increase over time

- Cash value accumulation that grows steadily

- Optional riders for additional protection

Best for: Individuals seeking stability, customizable premium options, and strong support from local agents.

AARP Whole Life Insurance

AARP members can access whole life insurance underwritten by a top-rated insurer. These policies offer permanent coverage with flexible options.

Key features:

- Lifetime coverage with predictable premiums

- Policies designed for members aged 50 and above

- Cash value accumulation for long-term financial planning

- Some plans offer guaranteed acceptance options

Best for: Older adults who want reliable coverage and added financial security backed by a reputable company.

Gerber Whole Life Insurance

Gerber Life offers straightforward whole life policies suitable for individuals and families. Policies include lifelong protection with cash value accumulation.

Key features:

- Permanent coverage with guaranteed death benefit

- Cash value grows over time and can be borrowed against

- Flexible coverage amounts to fit different budgets

- Easy application process

Best for: Families and individuals seeking reliable, lifelong protection with savings benefits.

Primerica Whole Life Insurance

Primerica primarily offers term life insurance rather than whole life policies. They focus on affordable term coverage paired with a philosophy of investing the difference in separate financial accounts.

Best for: Individuals who prefer term coverage with lower premiums and independent investment options rather than permanent life insurance.

Colonial Penn Whole Life Insurance

Colonial Penn specializes in guaranteed acceptance whole life insurance, ideal for older adults or those with health challenges.

Key features:

- No medical exam required

- Fixed premiums for life

- Coverage amounts typically suitable for final expenses

- Simplified application process

Best for: Seniors or individuals seeking coverage for final expenses without medical underwriting.

Quick Comparison Table

| Provider | Whole Life Offered | Underwriting | Best For |

| State Farm | Yes | Traditional, may include dividends | Full-featured permanent coverage with strong support |

| AARP | Yes | Traditional, membership-based | Members 50+ seeking reliable coverage |

| Gerber Life | Yes | Traditional permanent plans | Families and individuals seeking cash value growth |

| Primerica | No | N/A | Term protection and separate investments |

| Colonial Penn | Yes (guaranteed issue) | Guaranteed acceptance | Seniors or simplified issue policies for final expenses |

Whole Life Insurance by Audience

Whole Life Insurance is not a one-size-fits-all product. Different age groups and financial situations require tailored approaches to coverage. Understanding which policy suits your profile ensures optimal protection, cash value growth, and financial planning benefits.

Whole Life Insurance for Adults

Adults, especially those in their 20s to 50s, can benefit from Whole Life Insurance as both a protection tool and a long-term savings plan.

Key benefits for adults:

- Provides lifelong coverage for dependents and family security

- Builds cash value that can be accessed for emergencies, home purchase, or retirement supplement

- Fixed premiums help in budgeting and financial planning

- Offers potential dividends if choosing a participating policy

Best use: Adults with growing families, mortgages, or long-term financial goals who want both protection and wealth-building features.

Whole Life Insurance for Seniors

Seniors often have different priorities, focusing on estate planning, legacy, and final expense coverage. Whole Life Insurance can be a strategic tool even later in life.

Key benefits for seniors:

- Guaranteed acceptance options in some policies

- Coverage for funeral, medical, and outstanding debts

- Fixed premiums that do not increase with age

- Cash value can be used if needed for emergencies

Best use: Seniors looking for predictable lifelong coverage, simplified underwriting, and a way to leave a financial legacy.

If You Are 18 With No Debt or Dependents, Do You Need Life Insurance

At 18, if you have no debt, dependents, or financial obligations, life insurance is generally not an immediate necessity. However, some considerations may make it worthwhile:

- Lock in low premiums early: Buying a small whole life policy now can secure low rates for life

- Start building cash value: Early cash value growth can supplement long-term savings

- Future financial planning: As you acquire debt, family, or assets, having coverage already in place is beneficial

Best approach: Consider a small permanent policy for long-term financial growth, or wait until financial responsibilities increase to purchase adequate coverage.

Regional Whole Life Insurance Information

Whole Life Insurance policies can vary by country due to regulations, taxation, market practices, and available product features. Below is a clear, high‑quality guide focused specifically on Whole Life Insurance in Canada, written for readers and optimized for search engines.

Whole Life Insurance Canada

Whole Life Insurance in Canada is a permanent life insurance policy that provides lifelong protection, guaranteed premiums, and a guaranteed death benefit. It also builds a cash value component that grows over time, offering both protection and long‑term value for Canadian policyholders.

What Canadian Whole Life Insurance Offers

Lifetime Coverage

Canadian whole life policies guarantee protection for your entire life, as long as premiums are paid. This provides peace of mind for families and estate planning.

Cash Value Growth

Part of your premium goes into a cash‑value account that grows on a tax‑sheltered basis. Over time, this cash value can be accessed through policy loans or withdrawals to support major financial needs.

Fixed Premiums

Premiums are locked in at the start, so they will not increase with age or changing health. This predictability makes budgeting easier over the long term.

Tax Advantages

The cash value component grows tax‑sheltered. In Canada, accessing this value through policy loans may provide tax‑efficient funds for retirement, education, or emergencies.

Why Canadians Choose Whole Life Insurance

Long‑Term Financial Security

Whole life insurance offers protection that does not expire, making it ideal for long‑term financial planning and family security.

Estate Planning and Legacy

Canadians often use whole life policies to leave a legacy, cover estate taxes, or ensure financial support for beneficiaries.

Stable Savings Component

With a guaranteed cash value component, whole life insurance becomes a stable savings vehicle that can supplement retirement income or emergency funds.

Flexible Use of Cash Value

The cash value is not locked away. It can be used to pay premiums, support personal goals, or fund unexpected expenses through policy loans.

Policy Features Common in Canada

Participating Whole Life Policies

Many Canadian insurers offer participating whole life insurance, meaning policyholders may receive dividends. Dividends are not guaranteed but can enhance cash value and overall benefits.

Non‑Participating Whole Life Policies

These offer fixed benefits without dividends and often come with slightly lower premiums.

Extended/Universal Options

Some policies combine whole life insurance with flexible premiums or investment components, but the traditional whole life remains the most stable choice for guaranteed coverage.

Who Should Consider Whole Life Insurance in Canada

✔️ Individuals seeking guaranteed lifelong coverage

✔️ Those who want predictable premiums and cash value growth

✔️ Canadians focused on estate planning or legacy goals

✔️ People looking for a stable, tax‑sheltered savings element

Whole Life Insurance vs. Other Canadian Options

| Feature | Whole Life Insurance | Term Life Insurance |

| Coverage Duration | Lifetime | Fixed term (10–30 years) |

| Premium Stability | Fixed for life | Lower but increases at renewals |

| Cash Value | Yes, grows over time | No cash value |

| Estate Planning | Strong tool | No long‑term value |

| Best For | Long‑term security and savings | Short‑term protection |

Reviews, Opinions & Community Signals

Understanding public opinion and expert advice can help you make informed decisions about Whole Life Insurance and related financial products. This section summarizes community sentiment and expert guidance in an easy-to-read, high-value format.

Whole Life Insurance Reddit

Discussions on Reddit show a mix of praise and criticism for Whole Life Insurance, reflecting real user experiences.

Common observations:

- High Costs: Many users note that premiums for whole life insurance are significantly higher than term insurance, making it less attractive for younger or middle-income earners.

- Cash Value Growth: Some appreciate the cash value component, but others point out it grows slowly, and the policy may not break even for many years.

- Regret After Purchase: Several users regret purchasing whole life policies early, believing a term policy with separate investments could have been more beneficial.

- Specific Use Cases: Some acknowledge that whole life insurance works well for estate planning, long-term legacy planning, or for high-net-worth individuals.

Overall takeaway: Whole life insurance is useful in certain financial strategies, but many online communities favor term insurance paired with investment for better returns and flexibility.

Why Dave Says You Don’t Need Short-Term Disability Insurance

Financial expert Dave Ramsey advises against buying short-term disability insurance for most people, based on his philosophy of financial independence and efficient resource allocation.

Key reasons:

- Emergency Savings First: A well-funded emergency fund of three to six months’ expenses can cover short-term income loss, reducing the need for insurance.

- Employer Coverage: Many employers provide short-term disability benefits, making additional policies unnecessary.

- Cost vs Value: Premiums for short-term disability insurance may not be justified given the limited coverage period of 3–6 months.

- Focus on Long-Term Protection: Ramsey recommends prioritizing long-term disability insurance, which provides protection against serious, extended income loss.

Takeaway: Dave emphasizes self-insurance through savings and prioritizing policies that protect against significant, long-term financial risks rather than temporary setbacks.

Overall Community and Expert Insights

- Whole Life Insurance: Offers lifetime protection and cash value growth but can be costly; best for estate planning or long-term financial strategies.

- Reddit Consensus: Many users prefer term insurance combined with investments due to lower cost and higher flexibility.

- Short-Term Disability Insurance: Often unnecessary if you have emergency savings and employer coverage; long-term protection is more valuable.

Final Words

Whole Life Insurance provides both protection and savings, making it ideal for long-term financial security. Its predictable premiums, cash value growth, and estate planning benefits make it a trusted choice. Whether you are planning for family protection, retirement, or legacy, Whole Life Insurance ensures peace of mind and financial stability.

Frequently Asked Questions

What is Whole Life Insurance?

Whole Life Insurance is permanent life insurance providing lifelong coverage with a guaranteed death benefit and growing cash value.

How Does Whole Life Insurance Work?

It works by paying fixed premiums that build cash value over time while ensuring your beneficiaries receive a death benefit.

What Are the Benefits of Whole Life Insurance?

Benefits include lifelong protection, predictable premiums, cash value growth, tax advantages, and estate planning opportunities.

Who Should Buy Whole Life Insurance?

Individuals seeking long-term financial security, wealth transfer, and guaranteed lifetime coverage should consider Whole Life Insurance.

Is Whole Life Insurance Worth It?

It is worth it for those prioritizing permanent coverage, cash value accumulation, and legacy planning over short-term affordability.

How Much Does Whole Life Insurance Cost?

Premiums vary by age, health, and coverage amount; generally higher than term insurance but provide lifetime benefits and cash growth.

Can Whole Life Insurance Be Used for Retirement?

Yes, cash value can supplement retirement income or be used for emergencies, making it a flexible long-term financial tool.

What Happens to Whole Life Insurance Cash Value When I Die?

The cash value typically passes to beneficiaries or can be used to increase the death benefit depending on the policy structure.

Chriselle Lim is a passionate digital creator and lifestyle blogger based in California, USA. As the voice behind Blogzeno, she shares creative captions, inspiring Instagram bios, insightful celebrity stories, and simple insurance guides designed for everyday readers. Emily believes that words have the power to connect people whether it’s through a perfect caption or a helpful article.

With years of experience in online writing and content strategy, Emily’s mission is to make information both useful and enjoyable. Her work blends creativity with clarity, helping readers express themselves confidently and stay informed about what truly matters.

When she’s not writing, you’ll find her exploring photography, social media trends, and new ways to inspire digital creators worldwide. Follow her journey on Blogzeno — where creativity meets everyday life.