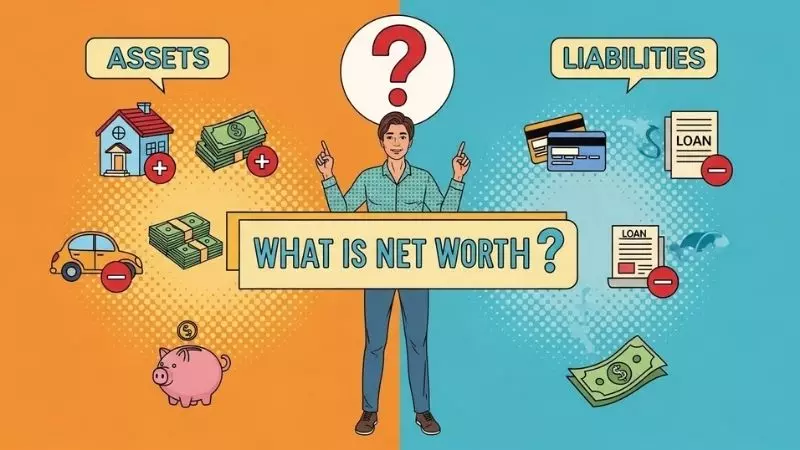

Net Worth is one of the most reliable indicators of your true financial position in today’s economy. It reflects the total value of your assets, including cash, property, investments, and savings, minus outstanding liabilities such as loans and credit card debt. Understanding net worth calculation helps individuals measure personal wealth, track financial growth, and plan long-term money management goals.

What Is Net Worth?

Net worth is the most practical way to understand your real financial standing in the modern economy. In simple terms, it shows what you truly own after subtracting everything you owe. Financial experts use net worth as a core metric to evaluate financial health, wealth accumulation, and long term money stability, making it far more reliable than income alone.

Think of net worth as a financial report card. It combines your assets, subtracts your liabilities, and gives you a clear number that reflects your current wealth position. Whether you are a beginner learning personal finance basics or someone planning long term wealth building, net worth provides a realistic picture that income figures often hide.

What counts as net worth?

Everything you own and owe plays a role in calculating net worth. Many people underestimate or overestimate their wealth because they do not know what should be included.

Assets included in net worth

- Cash and savings accounts

- Real estate property and land

- Investments such as stocks, mutual funds, and retirement accounts

- Vehicles with resale value

- Business ownership or side income assets

Liabilities included in net worth

- Home loans and mortgages

- Personal loans and student debt

- Credit card balances

- Car loans and installment plans

For accurate personal net worth calculation, always use current market values instead of purchase prices. This approach aligns with modern financial planning standards and improves decision making.

Assets vs liabilities (simple example)

To clearly understand how net worth works, let us look at a simple real life example. This method is commonly used in net worth calculation for beginners.

| Category | Example Items | Value |

| Assets | Savings, car, small investment | $50,000 |

| Liabilities | Loan, credit card debt | $20,000 |

| Net Worth | Assets minus liabilities | $30,000 |

This table shows that net worth is not about how much you earn, but about how much you keep after debts. Even with a moderate income, someone can build positive net worth by managing liabilities wisely.

Net worth vs money in the bank

Many people confuse net worth with the amount of money sitting in their bank account. While cash savings are important, they represent only one part of your overall financial picture.

Money in the bank shows liquidity, but net worth shows total financial strength. A person with low cash but valuable assets and minimal debt may have higher net worth than someone with large savings and heavy loans. This distinction is critical for long term financial planning, loan approvals, and investment readiness.

Understanding this difference helps readers avoid common financial mistakes and focus on sustainable wealth growth instead of short term cash accumulation.

Why net worth matters more than salary

Salary measures income flow, but net worth measures financial progress. High income does not guarantee wealth if spending and debt remain uncontrolled. That is why modern wealth advisors focus on net worth rather than monthly earnings.

Key reasons net worth matters more than salary:

- It reflects true wealth after expenses and debt

- It helps track financial improvement year by year

- It supports smarter investment and saving decisions

- It reveals long term financial security potential

For anyone aiming to improve financial independence, increase average net worth over time, or plan early retirement, tracking net worth provides clarity that salary figures simply cannot offer.

What Is the Top 5% Net Worth in the U.S.?

The top 5% net worth in the U.S. represents households that have accumulated significantly more wealth than the average American. This group is often used by economists and financial planners to define upper tier wealth status, not based on income, but on total assets minus liabilities. Understanding this benchmark helps readers set realistic financial goals and measure long term progress.

Unlike salary based rankings, net worth reflects real financial power, including investments, property, and equity growth. As inflation, housing prices, and investment returns change, the top 5% threshold also evolves, making it important to view these figures in a modern financial context.

How much net worth puts you in the top 5%?

To be in the top 5% of net worth in the United States, a household typically needs a net worth of approximately $2.5 million to $3 million or more. This range reflects recent financial data influenced by rising asset values and market performance.

This level of wealth usually includes diversified investments, real estate equity, retirement accounts, and minimal high interest debt. It is not defined by cash alone, but by the total value of long term assets that appreciate over time.

Top 5% net worth by age

Net worth expectations vary significantly by age due to earning years, investment time, and debt reduction. Below is a simplified age based view commonly used in wealth percentile analysis.

| Age Group | Approximate Top 5% Net Worth |

| Under 35 | $700,000+ |

| 35 to 44 | $1.5 million+ |

| 45 to 54 | $2.7 million+ |

| 55 to 64 | $4 million+ |

| 65+ | $5 million+ |

These figures highlight how compound growth and long term investing play a critical role in reaching top wealth brackets over time.

Top 5% vs top 10% vs top 1%

Understanding the difference between wealth tiers helps clarify where the top 5% truly stands.

- Top 10% net worth often starts around $1 million and reflects financial stability rather than elite wealth

- Top 5% net worth indicates strong asset accumulation and long term financial security

- Top 1% net worth usually exceeds $10 million and represents generational or investment driven wealth

The top 5% sits in a powerful middle ground. Wealthy enough to absorb economic shocks, but not necessarily part of the ultra rich class.

Is top 5% considered rich today?

In most financial discussions, being in the top 5% net worth bracket is considered rich by modern standards. This group typically enjoys financial flexibility, investment opportunities, and reduced reliance on earned income.

However, lifestyle perception varies by location and cost of living. In high cost cities, even top 5% households may not feel wealthy, while in average regions, this level of net worth often supports early retirement planning, passive income, and legacy wealth building.

Why top 5% wealth changed over time

The definition of top tier wealth has shifted due to multiple economic factors. Rising housing prices, stock market growth, inflation, and changes in retirement systems have all contributed to higher net worth thresholds.

Key reasons for change include:

- Long term stock market appreciation

- Real estate equity growth

- Inflation reducing purchasing power of money

- Increased access to investment platforms

As a result, reaching the top 5% net worth today requires smarter financial planning, disciplined investing, and a long term wealth mindset compared to previous generations.

How Many Americans Have a Net Worth of $1,000,000?

Understanding how many Americans have a net worth of $1,000,000 or more gives powerful insight into wealth distribution and financial success in the United States. Hitting the millionaire milestone today is not just about income, but disciplined saving, investing, and wealth building over time. For readers looking to improve personal financial standing, knowing where millionaires stand can be both motivating and realistic.

In recent financial studies, the definition of a millionaire focuses on total net worth, meaning the value of all assets minus all liabilities. This includes homes, retirement accounts, investments, business equity, and other valuable holdings. Let’s break down how common this level of wealth truly is across the U.S. population.

What percentage of Americans are millionaires?

Approximately 8 to 10 percent of American adults have a net worth of $1,000,000 or more. This figure can fluctuate slightly depending on economic conditions, asset values, and data sources, but consistently shows that millionaire status is noteworthy yet increasingly attainable with disciplined financial behavior.

Millionaire status here means net worth, not annual income. Some people can make high salaries but fall short of millionaire net worth due to high expenses or debt, while others reach seven figures by investing early and managing money wisely.

How common is a $1 million net worth?

A net worth of $1 million is still relatively uncommon compared to the total U.S. adult population, but it is growing due to rising investment values and broader access to financial markets. For perspective:

- Millions of households in the U.S. hold at least $1 million in total wealth

- Yet, the majority of American adults have net worth below this threshold due to student loans, housing costs, or limited retirement savings

This context helps readers see that hitting the $1 million mark is a major financial milestone that requires long term planning, not just a high income.

Millionaire households vs individuals

It is important to distinguish between millionaire households and millionaire individuals.

- Household net worth includes the combined wealth of all earners living in one home. Many statistics refer to households rather than single people

- Individual net worth focuses on a single person’s total assets minus liabilities

Because many households have two income earners or shared assets like property, the percentage of millionaire households tends to be higher than millionaire individuals.

Understanding this difference helps clarify how wealth is measured and reported in financial studies and surveys.

Millionaires by age group

Net worth tends to increase with age as people accumulate assets, pay down debts, and benefit from long term investment growth. The rough distribution of millionaires by age group often shows:

- Under 35 years old: Smaller percentage reach $1 million early, but numbers are rising with investment access

- 35 to 54 years old: Many achieve millionaire status through career growth and sustained saving

- 55 and older: Highest concentration of millionaires, often due to retirement accounts and real estate accumulation

This age progression highlights the importance of long term wealth building and compound growth, especially for those pursuing financial independence.

Is $1 million still a lot of money?

In today’s high cost economy, $1 million is a significant amount of wealth but its purchasing power depends on lifestyle and location. In some major cities with high housing costs, $1 million might not go as far as it once did, while in lower cost areas it can provide substantial financial security.

Despite changing economic conditions, many financial planners still view $1 million net worth as a major milestone because it usually signals strong savings habits, diversified investments, and a solid foundation for retirement planning or generational wealth. It remains a powerful motivational target for anyone working toward financial success.

How Many Americans Have $2 Million in the Bank?

Having $2 million in the bank sounds like the ultimate symbol of wealth, but in reality, very few Americans hold that much cash in a single or combined bank balance. Most high net worth individuals do not keep large sums idle in savings accounts. Instead, wealth is usually spread across investments, real estate, and diversified assets designed to grow over time.

This topic is often misunderstood because people confuse net worth with cash savings. Understanding this difference is essential for accurate financial education and realistic wealth expectations in today’s economy.

Net worth vs bank balance

A bank balance shows liquid cash, while net worth reflects total financial strength. This distinction is critical when discussing multimillion dollar wealth.

Key differences explained simply:

- Bank balance includes savings and checking accounts only

- Net worth includes cash plus investments, property, businesses, and equity

- A person can have high net worth with relatively low cash on hand

Most financially successful individuals focus on increasing total net worth, not keeping excessive money in banks where inflation reduces value.

How rare is $2 million in cash?

Holding $2 million in cash is extremely rare in the United States. Only a very small fraction of Americans have this level of liquid savings due to practical financial planning principles.

Reasons it is uncommon:

- Banks offer low returns compared to investments

- Inflation steadily erodes purchasing power

- Cash above emergency needs is usually reinvested

Even among millionaires, very few keep multiple millions sitting idle in bank accounts.

Do wealthy people keep money in banks?

Yes, wealthy individuals do keep money in banks, but usually for short term needs, not long term storage. Banks are used for liquidity, daily expenses, and emergency funds rather than wealth accumulation.

Common reasons rich people keep limited cash:

- Paying business or living expenses

- Managing short term opportunities

- Maintaining financial flexibility

High net worth individuals prioritize growth and capital efficiency over large cash balances.

Where rich people actually store wealth

Instead of holding millions in cash, wealthy people distribute assets across multiple categories to manage risk and growth.

Typical wealth storage includes:

- Stock market investments and index funds

- Real estate and rental properties

- Retirement and tax advantaged accounts

- Business ownership and private equity

- Bonds and alternative investments

This strategy protects wealth from inflation while creating long term financial stability.

Why cash-heavy net worth is uncommon

A cash heavy net worth is generally considered inefficient in modern financial planning. While cash provides safety and liquidity, too much of it can slow wealth growth.

Main reasons excessive cash is avoided:

- Inflation reduces real value over time

- Missed investment growth opportunities

- Lower overall financial performance

For this reason, financial advisors often recommend holding only enough cash for emergencies and planned expenses, while allowing the rest of wealth to work through diversified assets.

This approach aligns with how most financially successful Americans manage and grow their money.

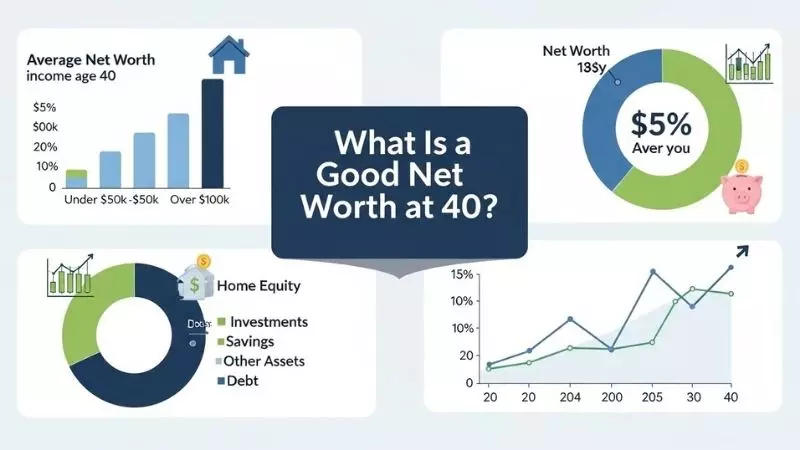

What Is a Good Net Worth at 40?

A good net worth at age 40 reflects how well someone has managed income, debt, saving, and investing during their prime earning years. By this stage of life, most people have settled careers, growing assets, and clearer financial goals. Net worth at 40 is often used by financial planners as a checkpoint for long term wealth building and retirement readiness.

Rather than comparing yourself only to averages, it is smarter to understand where you stand across different benchmarks like median, top percentages, and growth potential. This gives a more realistic and motivating picture of financial progress.

Average net worth at age 40

The average net worth at age 40 in the U.S. is significantly higher than what most people actually hold because averages are influenced by high net worth earners.

On average, Americans around age 40 have a net worth in the range of $450,000 to $600,000. This figure often includes:

- Home equity

- Retirement accounts like 401(k) or IRA

- Investments and savings

However, this number can be misleading, as it does not represent the typical individual due to wealth concentration at the top.

Median net worth at 40

The median net worth at age 40 provides a more accurate picture of the typical American. Median means half the population has more, and half has less.

For Americans around age 40, the median net worth is approximately $130,000 to $160,000. This lower figure reflects common realities such as:

- Mortgage debt

- Student loans

- Limited investment exposure

For most readers, the median is a more realistic comparison point than the average.

What net worth is considered good at 40?

A good net worth at 40 generally falls above the median and shows steady financial discipline. Financial educators often consider a net worth of $300,000 to $500,000 at age 40 as strong and healthy.

This level usually indicates:

- Consistent saving habits

- Growing retirement contributions

- Manageable debt levels

- Early stages of investment compounding

Reaching this range places someone on a solid path toward financial independence, even without extreme income.

Top 10% net worth at age 40

Being in the top 10% net worth at age 40 requires significantly higher asset accumulation. Individuals in this bracket typically have a net worth of $1 million or more by age 40.

This group often benefits from:

- Early investing and compound growth

- High savings rates

- Business ownership or strong equity positions

- Strategic debt management

Reaching the top 10% is not common, but it highlights what is possible with long term planning and disciplined financial behavior.

How net worth typically grows after 40

After age 40, net worth growth often accelerates if financial foundations are already in place. This phase benefits heavily from compound returns, higher peak earnings, and reduced debt.

Typical growth drivers after 40 include:

- Faster investment growth from larger portfolios

- Increased retirement contributions

- Mortgage balances decreasing

- Career income peaking

For many people, the most significant net worth gains happen between ages 40 and 60, making this stage critical for shaping long term financial security and retirement outcomes.

How to Find Out Someone’s Net Worth?

Finding out someone’s net worth can be straightforward for public figures but more complex for private individuals. Net worth is calculated as total assets minus liabilities, and for well-known personalities, this information is often estimated based on income, investments, and publicly available data. Understanding the difference between publicly available information and private financial privacy is critical before attempting to check someone’s wealth.

For readers curious about a person’s financial standing, it’s important to use credible sources and respect legal boundaries. Let’s explore the methods for both public figures and private individuals.

How to check a person’s net worth

To check someone’s net worth accurately, you must first determine if they are a public figure or a private individual.

- Public figures: Net worth estimates can be found in financial magazines, Forbes lists, and investment disclosures

- Private individuals: You may only access limited information through public filings, real estate ownership records, or business registrations, but detailed wealth is not publicly disclosed

Important tip: Always rely on credible sources; avoid rumors or unverified websites, as these can mislead.

How do you know the net worth of a person?

Knowing a person’s net worth involves analyzing both assets and liabilities. Key elements include:

- Real estate holdings

- Stock and investment portfolios

- Business ownership or shares

- Outstanding debts, loans, and liabilities

For public figures, most of this data is estimated using annual income, property filings, and company disclosures.

For private individuals, only general patterns like property ownership or business interest may be visible, so exact figures are usually confidential.

How to see how much a person is worth

You can see or estimate someone’s wealth depending on their public status:

- Public figures: Check trusted financial publications, celebrity wealth trackers, and investor reports

- Private individuals: Access public property records, business filings, and official documents where legally available

Online tools like Forbes Celebrity Net Worth, Wealth-X, and public financial disclosures for CEOs are commonly used for credible estimates.

Can you look up someone’s assets?

Yes, but with limitations:

- Public assets: Real estate ownership, corporate stakes, and certain investments may be publicly recorded

- Private assets: Bank accounts, personal investments, and debts are legally private and not publicly accessible

Attempting to access private financial accounts without consent is illegal, so only rely on lawful public information for net worth estimation.

Is someone’s net worth public record?

Net worth itself is not a public record. Only some elements of wealth may be public for certain individuals:

- Public figures (celebrities, CEOs): Financial details are often estimated from income, endorsements, stock holdings, and asset filings

- Private individuals (limits & legality): Net worth cannot be directly accessed. Legal methods include checking property ownership, business registrations, or court records for debts and liens, but exact figures remain private

Summary: Estimating net worth is legal for public figures using trusted sources, while for private individuals, respect privacy laws and use only publicly available information.

Can You Find the Net Worth of a Private Person?

Finding the net worth of a private person is very different from checking the wealth of celebrities or public figures. Private individuals are protected by privacy laws, so most of their financial information is not publicly accessible. Understanding what is legally available, what is not, and why online estimates are often inaccurate is essential for anyone researching personal wealth.

For readers, it’s important to approach this topic responsibly. Attempting to access private financial records without permission is illegal, and most “net worth” figures online for private individuals are speculative at best.

What information is public?

Even for private individuals, some financial information can be accessed legally through public records:

- Property ownership: Homes, land, and commercial real estate registered in public property databases

- Business ownership: Shareholding or directorships in registered companies

- Court records: Bankruptcy filings, liens, and judgments that reveal liabilities

- Professional disclosures: Certain professions may require asset reporting (e.g., financial advisors, politicians)

These sources provide partial insights but rarely give a complete picture of net worth.

What cannot legally be accessed?

Many key aspects of a private person’s finances are protected by law and cannot be accessed without consent:

- Bank accounts and balances

- Retirement accounts and investment portfolios

- Private debts and loans

- Insurance policies and personal trusts

Attempting to access these records without authorization is illegal and may result in criminal or civil penalties. Respecting privacy laws is crucial for ethical and legal research.

Why online estimates are often wrong

Online tools and websites sometimes claim to provide net worth for private individuals, but these estimates are often inaccurate. Reasons include:

- Incomplete information: They cannot access private accounts or debts

- Assumptions based on lifestyle: Inferring wealth from homes, cars, or vacations can be misleading

- Outdated data: Real estate, investments, and liabilities change frequently

Relying on these figures without verification can give a false sense of someone’s financial situation.

Estimated net worth vs verified data

It’s important to distinguish between estimated net worth and verified financial data:

- Estimated net worth: Calculated from public records, lifestyle clues, or online speculation. Useful for general context but not accurate

- Verified data: Comes from audited financial statements, legal filings, or disclosure reports. Only available for public figures or with explicit consent

For private individuals, only partial estimates are possible, and they should always be treated as approximations rather than confirmed facts.

Frequently Asked Questions About Net Worth

What net worth is considered rich in America?

In America, being considered rich usually means having a net worth in the top 5% to 10% of households, which is approximately $2.5 million to $3 million or more. Factors such as location, investments, and debt levels can influence this, meaning “rich” is relative.

Financial planners often advise aiming for a net worth that supports long-term wealth growth rather than just matching others.

Is net worth more important than income?

Yes, net worth is generally more important than income for assessing financial health. While income measures short-term earnings, net worth shows total assets minus liabilities, reflecting your true wealth.

Focusing on net worth encourages saving, investing, and reducing debt, which ultimately builds financial stability faster than high income alone.

How fast can net worth grow?

The speed at which net worth grows depends on income, savings, investments, and debt management. With smart financial planning, disciplined investing, and compound interest, many people can double their net worth over a decade or less.

Early investment, real estate equity, and stock market growth are key drivers of faster wealth accumulation.

What lowers net worth the most?

Several factors can significantly reduce net worth, including:

- High-interest debt like credit cards or payday loans

- Unplanned major expenses such as medical bills or home repairs

- Poor investment decisions or financial scams

- Lifestyle inflation where spending increases faster than income

Avoiding these pitfalls is crucial for maintaining and growing personal net worth over time.

Why most people misunderstand wealth

Many people confuse income, lifestyle, and net worth, thinking high salary equals wealth. True wealth is measured by assets minus liabilities, not how much money comes in each month.

Misunderstanding this can lead to overspending, debt accumulation, and slow progress toward financial independence. Educating yourself about net worth calculation and financial planning is essential to avoid this common mistake.

Chriselle Lim is a passionate digital creator and lifestyle blogger based in California, USA. As the voice behind Blogzeno, she shares creative captions, inspiring Instagram bios, insightful celebrity stories, and simple insurance guides designed for everyday readers. Emily believes that words have the power to connect people whether it’s through a perfect caption or a helpful article.

With years of experience in online writing and content strategy, Emily’s mission is to make information both useful and enjoyable. Her work blends creativity with clarity, helping readers express themselves confidently and stay informed about what truly matters.

When she’s not writing, you’ll find her exploring photography, social media trends, and new ways to inspire digital creators worldwide. Follow her journey on Blogzeno — where creativity meets everyday life.