Health insurance is a smart way to protect yourself from high medical costs, but many people still ask, how does health insurance work in real life. It helps cover expenses like doctor visits, hospital stays, prescription drugs, and preventive care by sharing the cost between you and your insurance provider.

When you pay a monthly premium, your health insurance policy gives you access to a network of healthcare services at lower rates. Understanding health insurance coverage, deductibles, copays, and claim processes makes it easier to choose the best health insurance plan for your needs and save money on medical bills.

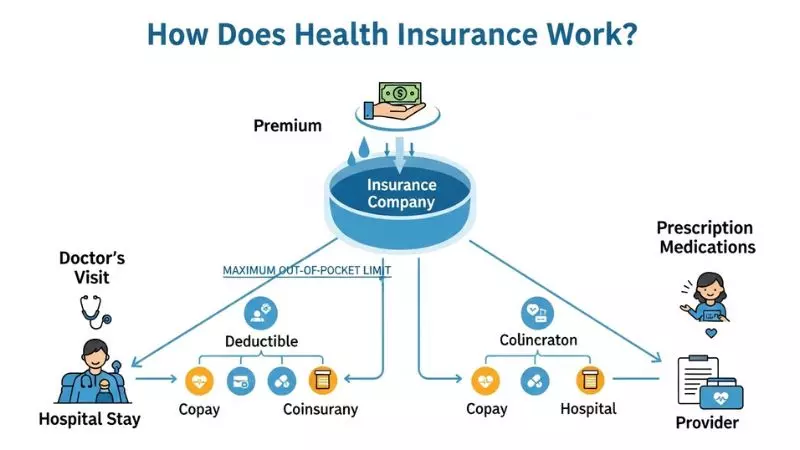

How Does Health Insurance Work?

Health insurance is a structured financial agreement between an individual and an insurance provider designed to cover medical expenses. Instead of paying the full cost of healthcare services, the policyholder shares the financial responsibility with the insurer.

The insured person pays a recurring premium, and in return, the insurance company contributes toward eligible medical costs such as doctor visits, hospitalization, prescription drugs, preventive care, and emergency treatment.

Health insurance policies in 2026 are more technology driven, offering digital claim processing, telemedicine access, wellness programs, and preventive care coverage to improve long term health outcomes.

Key Components of Health Insurance Coverage

Health insurance functions through several essential elements that define how costs are shared between the insured person and the insurance company.

- Premium

The fixed amount paid monthly or annually to maintain active coverage. - Deductible

The amount the policyholder must pay before the insurance company begins to contribute. - Copayment

A fixed charge paid at the time of receiving a service such as a doctor visit or prescription. - Coinsurance

The percentage of costs shared after the deductible has been met. - Provider Network

A group of hospitals and physicians approved by the insurance company. - Claim

A formal request for payment submitted to the insurer for medical services received.

Understanding these components allows policyholders to manage healthcare costs efficiently and avoid unexpected financial obligations.

Importance of Health Insurance in 2026

Healthcare costs continue to rise due to advanced treatments and technology based services. Health insurance protects individuals from financial exposure while supporting preventive and long term care.

- Coverage for medical emergencies.

- Access to quality healthcare providers.

- Protection from high hospitalization expenses.

- Support for mental health and wellness services.

- Integration with telehealth and digital medical platforms.

Health insurance enables individuals to focus on recovery rather than financial stress.

How Does Health Insurance Work?

The operational process of health insurance begins once a policy is active and premiums are paid consistently. When medical services are required, the insured individual visits a healthcare provider within the insurer’s approved network. The provider verifies coverage and submits a claim to the insurance company for payment.

The insurer reviews the claim based on the policy terms, calculates the covered amount, and determines the policyholder’s share. The insured person pays any required deductible, copayment, or coinsurance, and the insurance company pays the remaining approved balance.

Step by Step Insurance Process

- Select an appropriate health insurance plan.

- Maintain coverage through regular premium payments.

- Visit an in network healthcare provider.

- Present insurance identification.

- Receive medical services.

- Provider submits the claim.

- Insurer processes and pays the eligible portion.

This system ensures transparency and cost sharing between the patient and the insurance provider.

Essential Insurance Terminology

| Term | Description |

| Premium | Regular payment required to keep coverage active |

| Deductible | Amount paid before insurance contributions begin |

| Copayment | Fixed charge per medical service |

| Coinsurance | Percentage shared after deductible |

| Network | Approved healthcare providers |

| Claim | Request for reimbursement or direct payment |

These terms define financial responsibility and help policyholders plan medical expenses effectively.

How Does Health Insurance Work for Beginners?

For individuals new to healthcare coverage, health insurance provides financial security by reducing direct medical expenses. Beginners typically enroll in basic coverage plans that include outpatient care, emergency services, hospitalization, diagnostic tests, prescription medication, and preventive health screenings.

Instead of paying full treatment costs, policyholders contribute predictable premiums while the insurer manages major healthcare expenditures. This structure allows beginners to access quality medical care without significant financial strain.

Beginner Level Explanation

- Purchase a health insurance policy.

- Pay scheduled premiums.

- Use insurance when healthcare is needed.

- Pay a defined portion of the bill.

- Insurance covers the remaining eligible costs.

This approach simplifies healthcare budgeting and risk management.

What Beginners Should Evaluate

- Affordable premium rates with balanced deductibles.

- Comprehensive provider network access.

- Emergency and inpatient coverage.

- Prescription drug benefits.

- Telemedicine availability in modern plans.

Selecting the correct plan supports long term health and financial stability.

Common Beginner Errors

- Focusing only on low premium cost.

- Overlooking deductibles and cost sharing.

- Ignoring network limitations.

- Missing policy renewal deadlines.

- Not reviewing annual policy updates.

Avoiding these mistakes improves overall insurance utilization.

How Does Health Insurance Work for Dummies?

At its simplest level, health insurance is a cost sharing system designed to help pay for medical treatment. The insured individual pays a regular fee, and the insurance provider pays a substantial portion of medical expenses when care is required.

The objective is not complexity but protection. Insurance exists to reduce financial risk while ensuring consistent access to healthcare services.

Simplified Explanation

- Pay premiums regularly.

- Receive insurance coverage.

- Visit a doctor when needed.

- Provide insurance information.

- Pay a small portion.

- Insurance pays the larger portion.

Practical Example

If a medical bill totals $5,000 and the deductible is $500:

- The policyholder pays the first $500.

- The insurance company pays the remaining eligible amount according to the policy.

- The financial burden is significantly reduced.

Why Basic Health Insurance Matters

- Medical emergencies are unpredictable.

- Healthcare costs continue to increase.

- Insurance protects personal savings.

- It improves access to quality treatment.

- It provides financial and emotional security.

Health insurance, when understood properly, becomes a strategic tool for managing both health and financial responsibilities.

How Does Health Insurance Work with Deductibles?

A deductible is one of the most important cost sharing components in a health insurance plan. It represents the amount a policyholder must pay out of pocket before the insurance company begins covering eligible medical expenses. Understanding how deductibles work helps individuals manage healthcare budgets and avoid unexpected financial strain.

When a medical service is received, the cost is first applied to the deductible. Once the deductible is met, the insurer starts paying its portion according to the policy terms. Some services such as preventive care, annual checkups, and vaccinations may be covered before the deductible is reached, depending on the plan structure.

In modern health insurance plans in 2026, deductibles are designed to balance affordability with coverage, encouraging responsible healthcare usage while still protecting against major medical costs.

How Deductibles Function in Real Practice

- The policyholder selects a plan with a specific deductible amount.

- Medical bills are paid out of pocket until the deductible is met.

- After the deductible, insurance begins cost sharing.

- Copays or coinsurance apply once coverage starts.

- An annual reset usually applies to deductibles.

Why Deductibles Exist

- To reduce unnecessary medical spending.

- To keep monthly premiums affordable.

- To encourage preventive care awareness.

- To balance risk between insurer and insured.

- To control overall healthcare system costs.

Deductible Comparison Table

| Deductible Level | Premium Cost | Out of Pocket Risk | Best For |

| Low Deductible | Higher | Lower | Frequent medical users |

| Medium Deductible | Balanced | Moderate | Average healthcare needs |

| High Deductible | Lower | Higher | Healthy individuals with savings |

Choosing the correct deductible level improves both financial planning and healthcare access.

How Do Deductibles, Copays, and Coinsurance Work?

Deductibles, copays, and coinsurance form the foundation of cost sharing in health insurance. Each plays a different role in determining how much the policyholder pays versus how much the insurance company covers.

A deductible is paid first. After it is met, copays and coinsurance apply. Copays are fixed fees for services, while coinsurance is a percentage of the cost shared between the insured and the insurer.

Together, these elements create a structured payment system that keeps healthcare affordable while preventing overuse.

Step by Step Cost Sharing Process

- Pay medical bills until the deductible is reached.

- After deductible, apply copay or coinsurance.

- Insurance pays its share of the approved amount.

- The policyholder pays the remaining balance.

- Once the out of pocket maximum is reached, insurance pays fully.

Clear Comparison Table

| Feature | Deductible | Copay | Coinsurance |

| Purpose | Entry cost before coverage | Fixed visit fee | Percentage based cost |

| Payment Time | Paid first | Paid per visit | Paid after deductible |

| Example | $1,000 yearly | $30 per doctor visit | 20 percent of bill |

| Control Level | High financial impact | Predictable | Variable cost |

Why Understanding These Terms Matters

- Helps estimate yearly healthcare expenses.

- Prevents unexpected medical bills.

- Supports better plan selection.

- Improves claim accuracy.

- Enhances personal financial management.

Understanding how deductibles, copays, and coinsurance work gives policyholders confidence in using healthcare services wisely.

How Does Health Insurance Work Through an Employer?

Employer sponsored health insurance is one of the most common ways people receive medical coverage. In this model, the employer partners with an insurance provider to offer healthcare plans to employees. The company usually pays a portion of the premium, and the employee pays the remaining amount through payroll deductions.

This arrangement makes coverage more affordable and accessible compared to buying individual insurance plans. Employer plans often include broader benefits such as wellness programs, preventive care, mental health services, and telemedicine access in 2026.

Employer based health insurance creates a structured benefit system that supports employee health and workplace productivity.

How Employer Coverage Operates

- Employer selects insurance providers.

- Employees choose a plan during enrollment.

- Premiums are shared between employer and employee.

- Payroll deductions manage payments automatically.

- Employees use coverage for medical services.

Benefits of Employer Sponsored Insurance

- Lower premium costs due to employer contribution.

- Access to group negotiated rates.

- Broader provider networks.

- Integrated wellness and preventive programs.

- Simplified enrollment and billing process.

Employer Insurance Structure Table

| Feature | Employer Plan | Individual Plan |

| Premium Cost | Shared with employer | Fully paid by individual |

| Enrollment | Company scheduled | Anytime through marketplace |

| Coverage Options | Group benefits | Personal selection |

| Administration | Payroll handled | Self managed |

Employer sponsored insurance provides financial stability and organized healthcare access for employees.

How Does Health Insurance Work from an Employer?

When you receive health insurance from an employer, the company acts as the organizer of the insurance relationship. The employer negotiates plans, manages enrollment periods, and handles premium payments through payroll.

Employees review available plan options and select coverage that matches their healthcare needs. Once enrolled, coverage begins based on the employer’s policy schedule.

In modern systems, employer plans also include digital dashboards, online claim tracking, and telehealth access to simplify healthcare management.

Employer Plan Enrollment Process

- Employer announces open enrollment period.

- Employees review plan benefits.

- Select preferred coverage level.

- Payroll deductions begin automatically.

- Coverage becomes active on the assigned date.

What Employees Should Monitor

- Monthly payroll premium deductions.

- Deductible and copay structure.

- Network hospital access.

- Coverage updates each year.

- Dependent eligibility benefits.

Employer based insurance offers consistency and structured healthcare planning for working professionals.

How Does Health Insurance Work When Switching Jobs?

Switching jobs can impact health insurance coverage if not managed carefully. When employment ends, employer sponsored insurance typically remains active until the end of the coverage month. After that, the individual must arrange alternative coverage.

Many people transition to a new employer’s plan, a private policy, or temporary continuation coverage to avoid a gap in insurance.

In 2026, digital enrollment systems and marketplace platforms make job transition coverage faster and easier.

Coverage Options When Changing Jobs

- Enroll in the new employer’s health plan.

- Purchase an individual marketplace policy.

- Use temporary continuation coverage if available.

- Join a spouse’s insurance plan.

- Select short term health insurance if eligible.

Steps to Prevent Coverage Gaps

- Confirm the end date of current coverage.

- Compare new plan start dates.

- Enroll before leaving employment.

- Keep medical records accessible.

- Monitor claim processing during transition.

Managing insurance during job changes protects both health access and financial security.

How Does Health Insurance Work When You Retire?

Retirement changes health insurance eligibility and structure. Once employment ends permanently, employer sponsored coverage may stop unless retiree benefits are offered. Retirees must secure independent coverage to maintain healthcare access.

Many retirees move to government supported programs, private health plans, or supplemental insurance policies depending on age and location.

In modern healthcare systems, retirement coverage focuses on long term care, prescription drug benefits, chronic disease management, and preventive services.

Health Coverage Options After Retirement

- Government health programs based on age eligibility.

- Private individual insurance plans.

- Retiree health benefits from former employer.

- Supplemental coverage for gaps.

- Long term care insurance options.

Retirement Insurance Planning Tips

- Estimate healthcare costs early.

- Compare coverage before retiring.

- Budget for premiums and deductibles.

- Maintain continuous coverage.

- Review benefits annually.

Retirement health insurance planning ensures consistent access to medical care while protecting savings and long term financial stability.

How Does Health Insurance Work in the USA?

Health insurance in the United States operates through a mixed system of private insurers, employer sponsored plans, and government programs. Instead of a single national healthcare system, Americans obtain coverage through employers, private marketplaces, or public assistance programs depending on income, age, and employment status.

In the USA, health insurance works on cost sharing and risk pooling. Individuals pay premiums to maintain coverage, and when medical services are needed, the insurer shares the cost through deductibles, copays, and coinsurance. This structure allows policyholders to access healthcare while protecting against extreme medical expenses.

Modern U.S. health insurance in 2026 includes digital enrollment platforms, telehealth access, preventive care mandates, prescription drug coverage, mental health services, and online claim tracking for better user experience.

Core Structure of U.S. Health Insurance

- Individuals enroll through employers, marketplaces, or private providers.

- Monthly premiums maintain coverage.

- Deductibles apply before coverage begins.

- Copays and coinsurance determine cost sharing.

- Insurers pay remaining eligible costs.

- Annual out of pocket maximum limits personal expense.

Types of Health Insurance in the USA

| Type | Description |

| Employer Sponsored | Coverage provided through a workplace |

| Marketplace Plans | Policies purchased independently |

| Government Programs | Public health assistance coverage |

| Private Insurance | Direct plans from insurance companies |

| Short Term Coverage | Temporary medical insurance |

Why U.S. Health Insurance Is Unique

- Multiple provider options instead of one system.

- Strong role of private insurance companies.

- Emphasis on preventive healthcare coverage.

- Advanced digital healthcare services.

- Wide hospital and specialist networks.

Understanding how health insurance works in the USA helps individuals select appropriate coverage and manage healthcare costs responsibly.

How Does Health Insurance Work in California?

California follows the federal health insurance framework but operates its own state marketplace known as Covered California. Residents can purchase individual and family plans through this platform if they do not receive coverage from an employer.

California health insurance works through structured enrollment periods, income based subsidies, and standardized plan levels such as Bronze, Silver, Gold, and Platinum. These tiers determine premium cost and out of pocket responsibility.

In 2026, California plans focus heavily on telemedicine, mental health services, maternity care, and preventive screenings to improve population health outcomes.

How Coverage Works in California

- Residents enroll through Covered California or employers.

- Income based assistance may reduce premiums.

- Plan tiers define cost sharing structure.

- Deductibles and copays apply to services.

- Claims are processed digitally.

California Plan Levels Explained

| Level | Premium Cost | Out of Pocket Cost | Suitable For |

| Bronze | Lower | Higher | Healthy individuals |

| Silver | Moderate | Moderate | Average healthcare use |

| Gold | Higher | Lower | Frequent medical users |

| Platinum | Highest | Lowest | Ongoing medical care |

Benefits of California Health Insurance System

- State regulated consumer protections.

- Income based financial assistance.

- Comprehensive essential health benefits.

- Strong preventive care programs.

- Access to statewide healthcare networks.

California’s health insurance system balances affordability with quality healthcare access.

How Does Blue Cross Blue Shield Health Insurance Work?

Blue Cross Blue Shield (BCBS) is one of the largest health insurance networks in the United States, operating through independent regional companies. Instead of one single provider, BCBS consists of local plans that serve different states while sharing a nationwide provider network.

Blue Cross Blue Shield health insurance works by offering individual, employer, Medicare, and supplemental plans. Policyholders pay premiums, use in network providers, and share costs through deductibles, copays, and coinsurance based on their selected plan.

In 2026, BCBS plans integrate digital health tools, virtual doctor visits, prescription management, and fast claim processing for efficient healthcare delivery.

How BCBS Coverage Operates

- Choose a BCBS plan based on location.

- Pay monthly premiums.

- Use BCBS in network hospitals and doctors.

- Pay deductible and copay as required.

- BCBS covers eligible medical costs.

Key Features of Blue Cross Blue Shield

- Nationwide provider network access.

- Employer and individual coverage options.

- Medicare and supplemental plans.

- Digital claims and telehealth services.

- Prescription drug benefits.

BCBS Coverage Structure Table

| Feature | BCBS Plan |

| Coverage Type | Individual, employer, Medicare |

| Network Size | Nationwide access |

| Cost Sharing | Deductible, copay, coinsurance |

| Technology | Digital claims, telemedicine |

| Flexibility | Multiple plan levels |

Blue Cross Blue Shield health insurance provides structured, reliable healthcare coverage across the United States with modern service integration.

How Does Health Insurance Work in Other Countries?

Health insurance systems differ significantly around the world depending on government policy, population needs, and healthcare funding models. Unlike the United States, many countries use a universal healthcare structure where basic medical services are funded through taxes or mandatory insurance contributions.

In international systems, health insurance generally combines public coverage with optional private insurance for faster service access, additional benefits, or broader provider choice. The objective is to ensure affordable, accessible healthcare while controlling national healthcare costs.

By 2026, many countries have enhanced healthcare delivery using digital health cards, telemedicine platforms, centralized patient records, and streamlined reimbursement systems.

Global Health Insurance Models

- Tax funded universal healthcare systems.

- Mandatory national health insurance programs.

- Employer and employee contribution models.

- Public and private hybrid coverage.

- Optional supplemental insurance structures.

Comparison of International Healthcare Funding

| Model | Funding Source | Coverage Scope |

| Universal Tax System | Government taxes | Basic healthcare for all residents |

| Mandatory Insurance | Payroll contributions | Standard medical services |

| Hybrid System | Taxes plus private plans | Public care with private upgrades |

| Private Optional | Individual premiums | Expanded services and faster access |

These global models aim to balance cost efficiency, quality of care, and equitable access.

How Does Health Insurance Work in Canada?

Canada operates a publicly funded healthcare system known as Medicare. Instead of paying monthly premiums to private insurers for basic care, residents receive coverage funded through federal and provincial taxes. Each province administers its own health insurance plan under national standards.

Canadian health insurance covers essential medical services such as doctor visits, hospital stays, diagnostic tests, and surgeries. Private insurance is commonly used to supplement coverage for services not fully covered by the public system.

How Canadian Coverage Operates

- Residents register for provincial health insurance.

- Government funding covers basic healthcare.

- Patients present a health card at treatment.

- Providers bill the government directly.

- Supplemental private plans cover extras.

What Is Covered in Canada

| Covered Publicly | Usually Private |

| Doctor visits | Dental services |

| Hospital treatment | Vision care |

| Surgery | Prescription drugs outside hospitals |

| Diagnostic tests | Private hospital rooms |

Advantages of the Canadian System

- Universal healthcare access.

- No direct billing for core services.

- Strong preventive care focus.

- Financial protection for residents.

- Supplemental private flexibility.

Canada’s healthcare system prioritizes access and affordability for its population.

How Does Health Insurance Work in India?

India uses a mixed healthcare system combining public health programs and private health insurance. The government offers health schemes for lower income populations, while middle and upper income residents often purchase private insurance policies for broader coverage.

Health insurance in India works through annual premiums, deductibles, copays, and cashless hospital networks. Many insurers provide cashless treatment at network hospitals, reducing upfront payment needs.

In 2026, India’s health insurance sector emphasizes digital policy management, mobile claim filing, telemedicine, and expanded critical illness coverage.

How Insurance Works in India

- Individuals buy private health insurance policies.

- Premiums are paid annually.

- Network hospitals offer cashless services.

- Claims are submitted digitally.

- Insurers reimburse eligible expenses.

Common Coverage Areas in India

| Benefit | Coverage Type |

| Hospitalization | Inpatient treatment |

| Day care procedures | Same day surgeries |

| Critical illness | Specialized treatments |

| Pre and post hospitalization | Medical expenses around admission |

Benefits of Indian Health Insurance

- Access to private hospitals.

- Cashless treatment facilities.

- Affordable premium options.

- Expanding digital claim systems.

- Growing preventive care inclusion.

India’s model balances public support with private sector efficiency.

How Does Health Insurance Work in Australia?

Australia operates a universal healthcare system called Medicare, funded through taxes and a Medicare levy. Residents receive coverage for public hospital treatment, doctor consultations, and essential medical services.

Private health insurance is optional in Australia and is used to access private hospitals, shorter waiting times, and additional services such as dental and physiotherapy.

Australia’s health insurance system combines public healthcare security with private sector flexibility.

How Australian Healthcare Operates

- Residents enroll in Medicare.

- Government funds public healthcare services.

- Patients use Medicare cards for treatment.

- Private insurance supplements coverage.

- Claims are processed electronically.

Public vs Private Coverage in Australia

| Feature | Medicare | Private Insurance |

| Hospital Access | Public hospitals | Private hospitals |

| Waiting Time | Standard | Faster |

| Doctor Choice | Limited | Expanded |

| Extra Services | Basic | Dental and optical |

Strengths of the Australian System

- Universal healthcare availability.

- Public and private integration.

- Preventive health focus.

- Digital claim processing.

- Strong healthcare infrastructure.

Australia offers reliable healthcare coverage with personal choice options.

How Does Health Insurance Work in Germany?

Germany uses a mandatory health insurance system known as Statutory Health Insurance. Most residents are required to join public insurance funds, while high income earners may opt for private insurance.

German health insurance is funded through employer and employee payroll contributions. The system ensures universal access while maintaining competition among insurance funds.

In 2026, Germany emphasizes electronic health cards, centralized medical records, and efficient reimbursement management.

How German Insurance Works

- Residents enroll in statutory health funds.

- Contributions come from salary payments.

- Employers share premium costs.

- Electronic health cards manage access.

- Providers bill insurers directly.

German Coverage Structure

| Coverage Area | Included |

| Doctor visits | Yes |

| Hospital care | Yes |

| Prescription drugs | Partially |

| Preventive screenings | Yes |

Advantages of Germany’s Model

- Mandatory universal participation.

- Income based contributions.

- Strong provider networks.

- Efficient digital systems.

- High quality medical standards.

Germany’s system ensures stability, quality, and broad access to healthcare.

How Does Health Insurance Work in Ireland?

Ireland operates a public healthcare system supported by government funding, with private health insurance used for faster access and enhanced services. Residents are entitled to public hospital care, while many also purchase private coverage for additional benefits.

Irish health insurance works by combining tax funded services with voluntary private plans that reduce waiting times and expand hospital choices.

In 2026, Ireland continues improving digital patient systems, telemedicine access, and community based healthcare services.

How Irish Coverage Operates

- Residents access public healthcare services.

- Government funds hospital treatment.

- Patients may pay for some services.

- Private insurance supplements coverage.

- Claims are managed electronically.

Public and Private Comparison in Ireland

| Feature | Public System | Private Insurance |

| Hospital Access | Public hospitals | Private hospitals |

| Waiting Times | Longer | Shorter |

| Room Choice | Shared | Private |

| Extra Benefits | Basic | Expanded |

Benefits of Ireland’s Health Insurance Structure

- Universal public healthcare rights.

- Optional private coverage flexibility.

- Access to quality hospitals.

- Ongoing digital transformation.

- Patient focused healthcare services.

Ireland’s system balances public access with private efficiency to meet healthcare demands.

How Does Health Insurance Work? (Real People and Discussions)

Beyond official definitions, many people understand health insurance best through real life experiences and online discussions. Platforms such as forums, community boards, and social networks allow users to share how insurance actually works in daily life, including what surprises them, what saves them money, and what mistakes to avoid.

From these discussions, one theme is clear. Health insurance is not only about paying premiums, but about knowing how to use coverage properly. Real people often highlight the importance of understanding deductibles, networks, claims, and out of pocket limits before a medical emergency happens.

In 2026, with digital health portals, telemedicine, and mobile insurance apps, users are more involved in managing their healthcare than ever before. Learning from others helps new policyholders avoid confusion and unnecessary costs.

What Real Users Commonly Discuss About Insurance

- Confusion about deductibles and when coverage starts.

- Surprise bills from out of network providers.

- Importance of checking coverage before treatment.

- Claim delays and documentation mistakes.

- Using preventive care to reduce long term costs.

How Real Experiences Improve Insurance Decisions

| Area | Insight from Users |

| Plan Selection | Choose based on actual healthcare needs |

| Network Use | Always verify hospital and doctor network |

| Cost Control | Track deductible and out of pocket maximum |

| Claims | Keep records and digital copies |

| Prevention | Use free screenings and checkups |

By studying real user experiences, policyholders become more informed and confident when navigating health insurance systems.

How Does Health Insurance Work According to Reddit?

Reddit is one of the most active discussion platforms where people openly share how health insurance works in real situations. Subreddits related to personal finance, healthcare, and insurance contain thousands of posts explaining coverage problems, cost saving strategies, and claim handling experiences.

According to Reddit discussions, many users learn about health insurance only after facing a medical bill. These conversations emphasize that understanding policy details early prevents stress later.

Reddit users often describe insurance as a contract that rewards preparation. Those who read their plan documents, check networks, and monitor deductibles usually avoid financial trouble.

Common Lessons Shared on Reddit

- Always confirm whether a provider is in network before treatment.

- Track your deductible and out of pocket maximum.

- Do not ignore explanation of benefits statements.

- Use preventive services that are covered at low or no cost.

- Ask insurers for pre authorization on major procedures.

Realistic Example Shared in Discussions

Many Reddit users explain scenarios like this. A person with a $1,000 deductible receives a hospital bill of $4,000.

- The first $1,000 is paid by the patient.

- After the deductible, coinsurance applies.

- Insurance pays most of the remaining cost.

- The patient pays a small percentage.

- Total expense becomes manageable instead of overwhelming.

Why Reddit Discussions Matter for Beginners

- They show real billing situations.

- They highlight mistakes people commonly make.

- They explain insurance terms in simple language.

- They expose hidden costs and policy limits.

- They encourage proactive insurance management.

Learning how health insurance works according to Reddit gives beginners practical knowledge that goes beyond theory and helps them make smarter healthcare and financial decisions.

Frequently Asked Questions

How does health insurance work in simple terms?

Health insurance works by sharing medical costs between you and the insurer, where you pay a premium and the company covers most healthcare expenses after deductibles, copays, and coinsurance apply.

Is it better to have a $500 deductible or $1,000 health insurance?

A $500 deductible is better for frequent medical users, while a $1,000 deductible suits healthy individuals who prefer lower premiums and can manage higher out of pocket costs.

How does health insurance work for dummies?

You pay a monthly premium, visit an in network doctor when needed, pay a small portion, and your health insurance provider pays the remaining approved medical expenses.

How does health insurance work according to Reddit?

Reddit users explain health insurance as cost sharing where understanding networks, deductibles, and out of pocket limits early prevents surprise medical bills later.

How does health insurance work from an employer?

Employer health insurance works by sharing premiums between the company and employee, with payroll deductions managing payments while coverage includes network hospitals and cost sharing rules.

How does health insurance work with a deductible?

A deductible is the amount you pay first for medical services before health insurance starts covering eligible costs through copays and coinsurance.

How does health insurance work in the USA?

In the USA, health insurance works through private insurers, employers, and government programs where premiums, deductibles, copays, and networks determine medical cost sharing.

How does health insurance work with Blue Cross Blue Shield?

Blue Cross Blue Shield works by offering nationwide network plans where members pay premiums and share costs through deductibles, copays, and coinsurance for covered healthcare services.

How does health insurance work in California?

In California, residents enroll through Covered California or employers, choose tiered plans, and use cost sharing rules to access statewide healthcare provider networks.

How does health insurance work when you retire?

When you retire, employer coverage usually ends, so retirees move to government programs or private plans that cover healthcare through premiums and structured medical benefits.

Final Words: How Does Health Insurance Work

Understanding How Does Health Insurance Work helps individuals make informed healthcare and financial decisions before emergencies occur. Health insurance is built on cost sharing, where premiums keep coverage active and deductibles, copays, and coinsurance manage personal responsibility while insurers cover the majority of medical expenses.

In today’s digital healthcare environment, knowing How Does Health Insurance Work also means understanding networks, claims, preventive care, and coverage transitions such as job changes or retirement. With the right plan, people protect both their health and long term financial stability through smart insurance planning.

Chriselle Lim is a passionate digital creator and lifestyle blogger based in California, USA. As the voice behind Blogzeno, she shares creative captions, inspiring Instagram bios, insightful celebrity stories, and simple insurance guides designed for everyday readers. Emily believes that words have the power to connect people whether it’s through a perfect caption or a helpful article.

With years of experience in online writing and content strategy, Emily’s mission is to make information both useful and enjoyable. Her work blends creativity with clarity, helping readers express themselves confidently and stay informed about what truly matters.

When she’s not writing, you’ll find her exploring photography, social media trends, and new ways to inspire digital creators worldwide. Follow her journey on Blogzeno — where creativity meets everyday life.