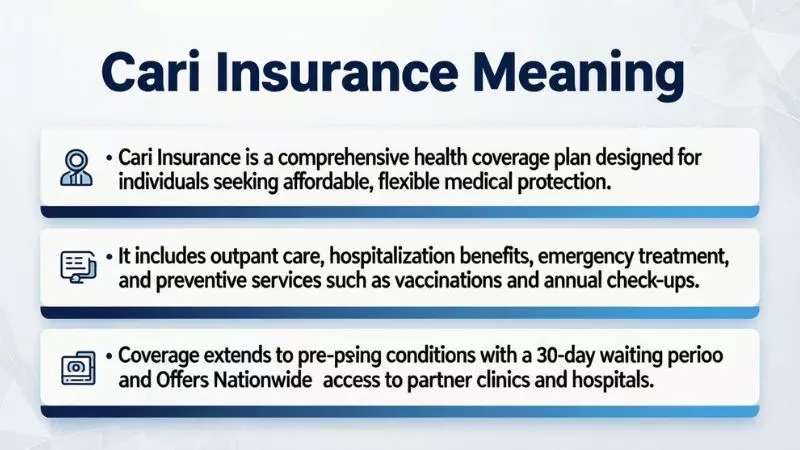

Cari Insurance Meaning refers to understanding what CARI insurance is, how it works, and why people use it for financial protection and risk coverage. Many users search for the cari insurance definition to learn about policy benefits, premium costs, claim process, and coverage types. If you are confused about what does cari insurance mean, this guide explains it in simple terms for beginners.

By knowing the real meaning of cari insurance, you can choose the right insurance plan for long term security and smart financial planning.

What Is CARI Insurance?

CARI Insurance stands for Contractors All Risk Insurance, a specialized policy designed to protect construction projects from unexpected financial loss. When people search for cari insurance meaning, they usually want to understand how builders, contractors, and project owners reduce risk during construction.

This insurance covers damage to property, materials, machinery, and even third-party liability caused by accidents, natural events, or human error.

In simple words, CARI insurance works as a safety net for construction projects, ensuring that work does not stop because of sudden repair costs or legal claims.

Key Benefits of CARI Insurance

- Protects buildings under construction from damage.

- Covers tools, materials, and construction equipment.

- Helps manage third-party injury or property damage claims.

- Reduces financial risk for contractors and project owners.

- Improves project credibility with investors and clients.

Who Needs CARI Insurance?

- Construction companies

- Civil engineers

- Project developers

- Building contractors

- Infrastructure investors

CARI insurance is especially important for large and small construction projects where financial exposure is high.

CARI Insurance Meaning

The CARI insurance meaning refers to a policy that offers all-risk coverage for construction activities, including on-site and off-site project risks. It protects against sudden physical loss or damage during the construction period, from the foundation stage to project completion.

When users ask what does CARI insurance mean, they are looking for clarity on how this policy manages construction uncertainty.

What Does CARI Insurance Cover?

- Fire and explosion damage

- Flood, storm, and natural disasters

- Theft of construction materials

- Accidental structural damage

- Equipment and machinery loss

- Third-party liability protection

What Is Usually Not Covered?

- Poor workmanship

- Normal wear and tear

- Intentional damage

- Project delay penalties

CARI Insurance Meaning in the Philippines

In the Philippines, the CARI insurance meaning focuses on protecting construction projects against risks common in the region such as typhoons, earthquakes, floods, and accidental damage. Many developers and contractors use CARI policies to meet regulatory and investor requirements.

People searching for cari insurance meaning in the Philippines often want to know how it supports local construction businesses and infrastructure development.

Why CARI Insurance Is Important in the Philippines

- High exposure to natural disasters.

- Growing real estate and infrastructure projects.

- Protection for contractors and property owners.

- Financial stability during project execution.

- Compliance with project financing standards.

Typical Coverage Scope in the Philippines

| Coverage Area | Purpose |

| Project Works | Protects the structure under construction. |

| Construction Materials | Covers loss of cement, steel, and fittings. |

| Machinery | Secures heavy equipment used on site. |

| Third Party Liability | Covers injury or property damage to others. |

| Natural Disaster Protection | Covers typhoons, floods, and earthquakes. |

Using CARI insurance in the Philippines helps contractors control risk while keeping projects running smoothly even after unexpected events.

CARI Insurance Meaning in Construction

The CARI insurance meaning in construction refers to full protection for every stage of a building project. From excavation to finishing, this policy secures the contractor against financial loss caused by accidents, site damage, and legal claims.

Search queries like cari insurance for construction projects show that users want reliable coverage during active work phases.

How CARI Works in Construction

- Starts when the project begins.

- Covers the site until completion or handover.

- Protects materials on and off the site.

- Includes liability for third-party injuries.

- Reduces project financial uncertainty.

Advantages for Construction Businesses

- Better risk management.

- Increased investor confidence.

- Fewer cash flow interruptions.

- Faster recovery after accidents.

- Improved legal protection.

CARI insurance meaning in construction is closely linked with builders risk insurance, contractor liability insurance, and project risk management solutions.

CARI Meaning in Construction Explained

The CARI meaning in construction explained simply means protecting a project from start to finish against unpredictable damage and liability. Construction projects involve heavy machinery, workers, and public interaction, which increases risk exposure. CARI insurance minimizes that exposure with structured financial coverage.

Step-by-Step Protection Flow

- Project registration under CARI policy.

- Risk evaluation of site and materials.

- Coverage activation from day one.

- Continuous protection during construction.

- Claim support in case of loss or damage.

When Should You Buy CARI Insurance?

- Before project excavation starts.

- When handling high-value materials.

- For multi-story buildings.

- During public infrastructure projects.

- When investors require risk coverage.

Quick Comparison for Better Understanding

| Without CARI Insurance | With CARI Insurance |

| Project owner pays all damages | Insurance handles major losses |

| High legal risk | Legal liability protection |

| Cash flow problems | Financial stability |

| Delayed project recovery | Faster repair and continuation |

Understanding the CARI meaning in construction helps contractors avoid major financial setbacks while ensuring long-term project success.

CARI Insurance in the Philippines

CARI Insurance in the Philippines is widely used in construction and infrastructure projects to protect contractors, developers, and project owners from unexpected financial losses. Because the country is exposed to natural hazards like typhoons, floods, and earthquakes, CARI insurance plays a major role in construction risk management.

When users search for CARI insurance in the Philippines, they want to know how this policy works locally, who needs it, and whether it is required for projects. The main goal of CARI coverage is to secure the project site, materials, equipment, and third-party liability from start to completion.

Why CARI Insurance Matters in the Philippines

- Protects projects from weather related damage.

- Reduces financial risk during construction.

- Supports investor and bank requirements.

- Covers third party injury and property damage.

- Keeps projects running after accidents or losses.

This makes CARI insurance a smart choice for both small and large scale construction developments in the Philippine market.

What Is CARI Insurance in the Philippines?

CARI insurance in the Philippines refers to a Contractors All Risk policy that provides comprehensive protection for construction works, materials, machinery, and legal liability while a project is ongoing. It is designed to cover sudden and accidental damage rather than predictable maintenance issues.

People searching for what is CARI insurance in the Philippines are usually contractors or developers who want coverage that fits local construction conditions and climate risks.

What Does It Typically Cover?

- Structural damage during construction.

- Loss of building materials on site.

- Damage to construction equipment.

- Fire, flood, storm, and earthquake risks.

- Third party injury or property damage claims.

What Makes It Useful Locally?

- Suitable for residential and commercial projects.

- Protects against disaster related losses common in the Philippines.

- Helps meet financing and contract requirements.

- Supports faster project recovery after incidents.

In short, CARI insurance in the Philippines works as a financial shield for construction projects facing environmental and operational risks.

Is CARI Insurance Mandatory in the Philippines?

Many users ask, is CARI insurance mandatory in the Philippines? The simple answer is that CARI insurance is not always legally required, but it is often contractually required by project owners, banks, and government funded projects.

Instead of being a general law, CARI insurance becomes mandatory based on agreements, financing rules, and risk management policies.

When CARI Insurance Is Required

- Bank financed construction projects.

- Government infrastructure developments.

- Large commercial buildings.

- Public private partnership projects.

- Investor backed real estate developments.

When It Is Optional but Recommended

- Small private residential builds.

- Low budget construction works.

- Short term renovation projects.

Practical View for Contractors

| Situation | Is CARI Required? |

| Bank funded project | Yes |

| Government construction | Yes |

| Private residential build | Usually no |

| Investor backed development | Yes |

| Small renovation work | Optional but smart |

Even when not legally mandatory, CARI insurance in the Philippines is considered best practice because it reduces disputes, protects cash flow, and increases project trust.

Who Needs CARI Insurance in Construction Projects?

CARI insurance is needed by anyone financially involved in a construction project. If you are responsible for materials, workers, equipment, or public safety, this policy helps protect your investment and legal position.

Users searching for who needs CARI insurance in construction projects want clarity on responsibility and risk coverage.

Parties That Should Have CARI Insurance

- Project owners and developers.

- Main contractors and subcontractors.

- Construction companies.

- Engineering firms.

- Infrastructure investors.

- Property development firms.

Why These Groups Need It

- To avoid large repair costs.

- To protect against third party lawsuits.

- To secure materials and equipment.

- To maintain stable cash flow.

- To increase credibility with partners and lenders.

Simple Risk Breakdown

| Role | Risk Without CARI | Benefit With CARI |

| Developer | Pays for damages personally | Insurance covers major loss |

| Contractor | Legal and repair exposure | Liability protection |

| Investor | Financial instability | Project security |

| Engineer | Operational risk | Coverage during execution |

In simple terms, if you build, manage, finance, or supervise a construction project, CARI insurance is essential for smart risk control and long term success.

CARI Insurance Cost & Computation

Understanding CARI insurance cost and computation helps contractors and developers plan project budgets accurately. Many users searching for CARI insurance price want to know what affects the premium and how insurers calculate the final amount. The price of Contractors All Risk insurance is not fixed because it depends on project value, location, construction type, duration, and risk exposure.

In simple terms, the higher the project risk and value, the higher the CARI insurance premium. Insurers evaluate the construction scope, materials, environmental hazards, and liability exposure before issuing a quotation.

Main Factors That Affect CARI Insurance Cost

- Total contract price or project value.

- Location and natural disaster exposure.

- Type of structure and construction method.

- Project duration and timeline.

- Coverage limits and extensions.

- Third party liability amount.

These elements shape how affordable or premium your CARI insurance policy will be.

CARI Insurance Price Explained

The CARI insurance price represents the premium paid to protect a construction project from accidental damage and liability claims. When users ask about cari insurance price explained, they want transparency on where the cost comes from and how insurers assess risk.

Instead of a flat fee, CARI insurance is usually charged as a percentage of the project cost.

What Goes Into the Price

- Contract works value.

- Cost of materials and equipment.

- Machinery and tools on site.

- Third party liability limit.

- Risk profile of the project area.

Typical Pricing Structure

| Cost Element | How It Affects Price |

| Project Value | Higher value means higher premium |

| Project Location | Disaster prone areas increase cost |

| Coverage Scope | Wider protection costs more |

| Project Duration | Longer projects cost more |

| Liability Limit | Higher limit raises premium |

CARI insurance price also depends on optional add ons such as maintenance coverage, testing period, and advanced liability extensions.

How Is CARI Insurance Computed?

Many users search how is CARI insurance computed to understand the calculation process before requesting quotes. Insurance companies follow a risk based pricing model.

Step by Step CARI Insurance Computation

- Determine total project cost.

- Assess site and environmental risk.

- Evaluate construction type and materials.

- Add machinery and equipment values.

- Include third party liability limits.

- Apply insurer premium rate percentage.

Simple Computation Formula

CARI Premium = Project Value × Rate Percentage + Extensions Cost

Sample Computation Table

| Item | Example Amount |

| Project Value | PHP 50,000,000 |

| Premium Rate | 0.30 percent |

| Base Premium | PHP 150,000 |

| Liability Extensions | PHP 25,000 |

| Estimated Total Premium | PHP 175,000 |

This table helps users see how contractors all risk insurance is computed in a practical and transparent way.

How Much Is Contractors All Risk Insurance in the Philippines?

When people ask how much is contractors all risk insurance in the Philippines, they usually want a realistic price range. In the Philippine market, CARI insurance premiums commonly range between 0.20 percent to 0.60 percent of the total project value, depending on risk factors.

Average CARI Insurance Cost Range

| Project Size | Estimated Premium Range |

| Small Project (PHP 5M) | PHP 10,000 to PHP 30,000 |

| Medium Project (PHP 20M) | PHP 40,000 to PHP 120,000 |

| Large Project (PHP 100M) | PHP 200,000 to PHP 600,000 |

What Makes Philippine Pricing Different

- Exposure to typhoons and earthquakes.

- Urban vs provincial project locations.

- Type of building such as residential, commercial, or infrastructure.

- Duration of construction period.

- Third party liability requirements.

To get the best price for CARI insurance in the Philippines, contractors should compare quotes, adjust coverage limits wisely, and disclose project details accurately to insurers.

CARI Insurance Requirements & Policy Details

Understanding CARI insurance requirements and policy details is essential before purchasing a Contractors All Risk policy. Many users searching for CARI insurance policy requirements want to know what documents are needed, how coverage works, and what conditions apply. Insurers evaluate your project profile, risk exposure, and legal responsibilities before issuing the policy.

In simple words, CARI insurance is not just a formality. It is a structured agreement that defines how your construction project is protected from financial loss, damage, and liability claims.

Why Requirements and Policy Details Matter

- Ensures accurate risk assessment.

- Prevents claim rejection later.

- Defines legal protection scope.

- Helps contractors meet bank and investor rules.

- Improves project compliance and transparency.

Knowing these details early saves time, money, and future disputes.

CARI Insurance Requirements Checklist

The CARI insurance requirements checklist helps contractors and developers prepare everything insurers need to underwrite the policy. When users search CARI insurance requirements checklist, they want a clear list they can follow before applying.

Basic CARI Insurance Requirements

- Project contract value and scope of work.

- Construction site location details.

- Project timeline and duration.

- List of machinery and equipment values.

- Construction method and materials used.

- Third party liability limits.

- Contractor and subcontractor information.

Supporting Documents Often Required

- Approved project plans.

- Bill of quantities.

- Construction schedule.

- Company registration documents.

- Safety and risk management plan.

Quick Preparation Table

| Requirement | Purpose |

| Project Value | Sets premium computation base |

| Site Location | Determines environmental risk |

| Timeline | Defines coverage period |

| Equipment List | Adds machinery protection |

| Liability Limit | Covers third party exposure |

Completing this checklist ensures faster approval and accurate CARI insurance pricing.

Contractor All Risk Insurance Policy Terms and Conditions

The contractor all risk insurance policy terms and conditions define how coverage applies and when claims are accepted or rejected. Users searching CARI policy terms and conditions want clarity to avoid future misunderstandings.

These terms form the legal agreement between the insurer and the insured contractor.

Common Policy Terms Explained

- Policy period begins from project start date.

- Coverage ends upon project completion or handover.

- Only sudden and accidental damage is covered.

- Exclusions include wear and tear and faulty design.

- Deductibles apply to every claim.

- Claims must be reported within policy timelines.

Important Conditions Contractors Should Know

- Accurate project disclosure is required.

- Safety measures must be followed on site.

- Unauthorized project changes may affect coverage.

- Maintenance extensions need separate approval.

Key Term Overview

| Term | Meaning |

| Deductible | Amount paid by contractor before insurance |

| Policy Period | Time coverage remains active |

| Exclusion | Risks not covered by policy |

| Endorsement | Added coverage extension |

| Claim Notification | Time allowed to report loss |

Understanding these contractor all risk insurance policy terms and conditions helps prevent denied claims and legal disputes.

What Does a CARI Insurance Policy Cover?

Many users ask, what does a CARI insurance policy cover? The answer is that it provides broad protection for construction works, materials, machinery, and liability during the building phase.

Main Coverage Areas

- Damage to buildings under construction.

- Loss of construction materials on site.

- Damage to machinery and equipment.

- Fire, flood, storm, and earthquake risks.

- Theft and accidental destruction.

- Third party bodily injury and property damage.

Optional Coverage Extensions

- Testing and commissioning period.

- Maintenance period protection.

- Off site storage coverage.

- Professional fees for redesign.

- Debris removal expenses.

Coverage Comparison Table

| Coverage Type | Included in CARI |

| Project Works | Yes |

| Materials on Site | Yes |

| Machinery | Yes |

| Natural Disaster Risks | Yes |

| Third Party Liability | Yes |

| Normal Wear and Tear | No |

A well structured CARI insurance policy protects contractors from major financial losses while supporting smooth project completion.

Contractors All Risk Insurance Explained

Contractors All Risk Insurance, often called CARI insurance, is a comprehensive policy designed to protect construction projects from unexpected financial loss. Users searching for contractors all risk insurance explained want a clear understanding of how this coverage works, who needs it, and what risks it manages during construction.

This insurance protects not only the physical structure being built but also materials, equipment, and third party liability. It supports contractors, developers, and investors by reducing exposure to accidents, natural disasters, and operational mistakes that could otherwise stop a project.

Why Contractors All Risk Insurance Matters

- Secures project investment from start to completion.

- Protects materials and machinery on site.

- Covers legal liability to third parties.

- Supports financial stability during construction.

- Improves trust with banks and partners.

Understanding contractors all risk insurance is key for smart construction risk management and long term project success.

Contractors All Risk Insurance Meaning

The contractors all risk insurance meaning refers to a policy that offers broad all risk coverage for construction projects, protecting against sudden and accidental loss or damage during the building phase.

When people search contractors all risk insurance meaning, they want to know how it differs from basic insurance and why it is important for contractors.

What the Policy Means in Practice

- Covers buildings under construction.

- Protects materials and equipment.

- Includes liability for injury and property damage.

- Applies from project start to completion.

- Covers unexpected and accidental events.

Simple Definition Table

| Term | Meaning |

| Contractors All Risk | Insurance for construction project protection |

| All Risk | Covers most accidental damages except listed exclusions |

| Liability | Legal responsibility to third parties |

| Coverage Period | Time the project is insured |

In short, contractors all risk insurance meaning is about full financial protection for construction activity risks.

Difference Between CARI Insurance and Contractors All Risk Insurance

Many users ask about the difference between CARI insurance and contractors all risk insurance. The truth is that there is no real difference in coverage. CARI is simply the abbreviated name of Contractors All Risk Insurance.

However, people still search this phrase to understand if any technical difference exists.

Key Clarification

- CARI insurance is short form of Contractors All Risk Insurance.

- Coverage scope is the same.

- Both protect construction works and liability.

- Both include materials, machinery, and third party risk.

Comparison Table

| Feature | CARI Insurance | Contractors All Risk Insurance |

| Meaning | Abbreviation | Full policy name |

| Coverage | Same | Same |

| Usage | Common term | Formal term |

| Protection Scope | Identical | Identical |

So when users compare CARI insurance vs contractors all risk insurance, they are really comparing the same construction risk protection policy under two different names.

What Risks Are Covered Under Contractors All Risk Insurance?

Users searching what risks are covered under contractors all risk insurance want a list of real world dangers that the policy handles during construction.

Major Risks Covered

- Fire and explosion damage.

- Flood, storm, and earthquake loss.

- Theft of construction materials.

- Accidental structural damage.

- Machinery and equipment breakdown.

- Third party injury and property damage.

Operational Risks

- Collapse during construction.

- Impact damage from vehicles.

- Water damage from faulty installations.

- Human error during building work.

Risk Coverage Table

| Risk Type | Covered |

| Fire and Explosion | Yes |

| Natural Disasters | Yes |

| Theft | Yes |

| Accidental Damage | Yes |

| Wear and Tear | No |

| Intentional Damage | No |

Contractors all risk insurance protects projects from high impact financial threats while excluding predictable or intentional losses.

Common Car Insurance Terms Explained

Understanding common car insurance terms is essential for every vehicle owner. Many users searching for car insurance meaning terms want clarity on confusing phrases, abbreviations, and policy details. Knowing these terms helps you choose the right coverage, avoid claim rejections, and manage premiums effectively.

Car insurance, vehicle insurance, and auto insurance may sound similar but involve subtle differences in terms and coverage. Being familiar with terms like supplement, CAP, and liability definitions can make your insurance experience smoother.

Why Knowing Car Insurance Terms Matters

- Prevents misunderstandings with insurers.

- Helps you select the right coverage type.

- Clarifies claim processes and payout expectations.

- Improves decision-making for premium optimization.

- Protects you legally during accidents.

What Does Supplement Mean in Car Insurance?

In car insurance, supplement refers to an additional coverage or rider added to your base policy to extend protection. People searching what does supplement mean in car insurance are often looking for ways to enhance their standard policy without buying a completely new one.

Key Points About Supplements

- Supplements provide extra financial coverage beyond standard limits.

- Common supplements include roadside assistance, natural disaster coverage, and personal accident riders.

- Adding supplements may slightly increase your premium but significantly increases protection.

Example Table of Common Supplements

| Supplement Type | Purpose |

| Roadside Assistance | Help during breakdowns or emergencies |

| Natural Disaster Cover | Covers damages from floods, storms, earthquakes |

| Personal Accident Rider | Provides medical coverage for driver/passengers |

| Theft Protection | Additional compensation if car is stolen |

Using supplements effectively ensures that your car insurance covers unique risks specific to your needs.

What Does CAP Stand for in Insurance?

CAP in insurance commonly stands for Claim Assessment Procedure or Capital Adequacy Principle, depending on the context. Users searching what does CAP stand for in insurance usually want a clear understanding of how insurers evaluate claims or maintain financial stability.

CAP Explained in Simple Terms

- Claim Assessment Procedure: The method insurers use to assess and approve claims.

- Capital Adequacy Principle: Ensures insurance companies maintain enough reserves to pay future claims.

Why CAP Matters

- Ensures fair claim settlement.

- Protects policyholders against insurer insolvency.

- Standardizes claim evaluation processes.

- Helps avoid delays in claim payouts.

Knowing the CAP term can save policyholders from misunderstandings during claims or policy renewal.

Car Insurance vs Vehicle Insurance vs Auto Insurance

Many people search car insurance vs vehicle insurance vs auto insurance to understand whether these terms are different or interchangeable.

Key Differences

- Car Insurance: Typically refers specifically to coverage for personal cars or private vehicles.

- Vehicle Insurance: A broader term that includes motorcycles, trucks, commercial vehicles, and buses.

- Auto Insurance: Another general term for any motor vehicle insurance, often used internationally.

Quick Comparison Table

| Term | Scope | Common Usage |

| Car Insurance | Personal cars | Daily drivers, private owners |

| Vehicle Insurance | Cars, trucks, motorcycles | Broader insurance for multiple vehicle types |

| Auto Insurance | Cars, motorcycles, vans | International term, general usage |

Insurance Terminology & Meanings

Understanding insurance terminology and meanings is critical for policyholders, investors, and anyone exploring financial protection options. Many users search for terms like policy holder, CRIS, insurance carrier, and insurance company meaning to avoid confusion while buying or renewing insurance.

Insurance terms define your rights, responsibilities, and the scope of coverage. Familiarity with these terms ensures smooth policy management, accurate claim processing, and better financial planning.

Why Learning Insurance Terms Matters

- Clarifies who is responsible for the policy.

- Explains the scope of coverage and liability.

- Helps avoid disputes during claims.

- Improves understanding of financial protection.

- Supports informed decision-making for premiums and policies.

Policy Holder for Insurance Meaning

A policy holder in insurance is the person or entity that owns an insurance policy and is entitled to the benefits and obligations under it. Users searching policy holder for insurance meaning want to know who is legally responsible for paying premiums and filing claims.

Key Points

- Can be an individual, business, or organization.

- Holds the right to make changes to the policy.

- Receives benefits in case of claims.

- Must pay premiums to keep the policy active.

Example Table

| Term | Meaning |

| Policy Holder | Owner of the insurance policy |

| Insured | Person covered under the policy (can be different from holder) |

| Beneficiary | Receives payout in case of claim |

| Premium Payer | Responsible for paying insurance fees |

Knowing the policy holder definition helps in understanding legal and financial responsibilities in insurance contracts.

What Is an Insurance Policy Holder?

An insurance policy holder is essentially the legal owner of the insurance contract, responsible for maintaining the policy, paying premiums, and making claims. This term is often searched by beginners who want clarity between insured person and policy holder.

Responsibilities of a Policy Holder

- Paying regular premiums on time.

- Updating personal or business information.

- Filing claims when required.

- Choosing coverage limits and riders.

- Ensuring compliance with policy terms and conditions.

Understanding who the policy holder is ensures accountability and reduces confusion during claim settlements.

What Does CRIS Stand for in Insurance?

CRIS in insurance commonly stands for Credit Risk Insurance System or Customer Risk Information System, depending on context. Users searching CRIS meaning in insurance usually want to understand its role in evaluating risk or customer credit profiles.

Key Points About CRIS

- Helps insurers assess financial and credit risk of policyholders.

- Standardizes risk evaluation for faster approvals.

- Reduces potential claim defaults.

- Improves decision-making for premium pricing.

Knowing the meaning of CRIS helps policyholders understand how insurers calculate risk and eligibility for certain coverage types.

Insurance Carrier Meaning in Urdu

An insurance carrier is the company or entity that provides insurance coverage and assumes financial risk. In Urdu, it is often referred to as:

انشورنس فراہم کرنے والی کمپنی

Key Points

- Responsible for issuing the policy.

- Handles claims processing and payouts.

- Manages policyholder records and risk assessment.

- Often synonymous with insurance company or insurer.

Understanding the insurance carrier meaning in Urdu or local context ensures clarity for non-English speakers purchasing policies in Pakistan or other regions.

Insurance Company Name Meaning Explained

The insurance company name meaning refers to the legal and official title of the company providing the insurance policy. Many users search this to verify legitimacy or understand branding.

Key Points

- Identifies the insurer legally responsible for coverage.

- Used in all legal documents, claims, and communications.

- May include words like “Insurance”, “Assurance”, or “Mutual”.

- Helps distinguish between carriers, agents, and brokers.

Quick Table Example

| Term | Explanation |

| Insurance Company | Legal entity providing coverage |

| Insurance Carrier | Assumes financial risk and manages claims |

| Broker/Agent | Intermediary facilitating the policy |

| Policy Name | Specific insurance plan offered |

Frequently Asked Questions

What is Cari insurance meaning in simple words?

Cari insurance meaning is a policy that protects construction projects, materials, and equipment from accidental loss or damage during the building process.

How does CARI insurance work for contractors?

CARI insurance works by covering financial losses due to accidents, natural disasters, or third-party claims while a construction project is ongoing.

What does CARI insurance cover in construction projects?

It covers project works, machinery, materials, theft, fire, natural disasters, and third-party liability, ensuring smooth project completion.

Is CARI insurance mandatory for construction projects?

CARI insurance is not always legally mandatory but is often required by banks, investors, or government contracts for risk management.

How much does CARI insurance cost in the Philippines?

The premium is usually 0.20 to 0.60 percent of the total project value, depending on risk, location, project size, and coverage extensions.

Who needs CARI insurance for construction?

Project owners, main contractors, subcontractors, engineers, and investors need CARI insurance to protect financial and legal interests.

Can CARI insurance cover natural disasters?

Yes, most policies include coverage for floods, typhoons, earthquakes, and other accidental natural events affecting the construction site.

How long does CARI insurance last?

CARI insurance coverage typically lasts from project start to completion, including optional maintenance or testing periods if extended.

Conclusion

Understanding Cari Insurance Meaning is essential for contractors, developers, and project owners to manage construction risks effectively. This policy safeguards project works, materials, machinery, and liability against accidental damage and unforeseen events.

With a clear grasp of Cari Insurance Meaning, stakeholders can make informed decisions about coverage, premiums, and risk management, ensuring financial protection and smooth project completion. Investing in this insurance helps avoid costly setbacks and builds confidence for all parties involved in construction projects.

Chriselle Lim is a passionate digital creator and lifestyle blogger based in California, USA. As the voice behind Blogzeno, she shares creative captions, inspiring Instagram bios, insightful celebrity stories, and simple insurance guides designed for everyday readers. Emily believes that words have the power to connect people whether it’s through a perfect caption or a helpful article.

With years of experience in online writing and content strategy, Emily’s mission is to make information both useful and enjoyable. Her work blends creativity with clarity, helping readers express themselves confidently and stay informed about what truly matters.

When she’s not writing, you’ll find her exploring photography, social media trends, and new ways to inspire digital creators worldwide. Follow her journey on Blogzeno — where creativity meets everyday life.