Understanding the net worth of average American gives a clear picture of financial health across the country. From savings and investments to debts and home equity, knowing the typical wealth distribution in the US helps you compare your finances and plan smarter for the future. Many people are surprised to learn how factors like age, income level, and lifestyle choices impact the average net worth.

In 2026, the average American household net worth reflects growing trends in real estate, retirement accounts, and personal debt. Tracking these numbers using financial planning tools and wealth calculators can help individuals set realistic goals, improve savings, and make informed investment decisions. Discovering the real financial picture of Americans today can motivate you to take action and secure long-term financial stability.

What is the Real Net Worth of an Average American? (Surprising Numbers!)

Understanding the net worth of an average American goes beyond just checking bank balances. Net worth includes assets like homes, savings, and investments, minus liabilities such as loans, credit card debt, and mortgages. Surprisingly, many Americans overestimate their wealth because debts often reduce the actual financial picture significantly.

Key points to understand:

- Assets vs Liabilities: Home equity and retirement accounts are major contributors to net worth.

- Income vs Wealth: High income does not always translate to high net worth due to spending habits.

- Regional Differences: Americans in certain states have higher average net worth due to property values and local economies.

Knowing your real net worth helps in making smarter financial decisions, improving wealth management, and planning for retirement.

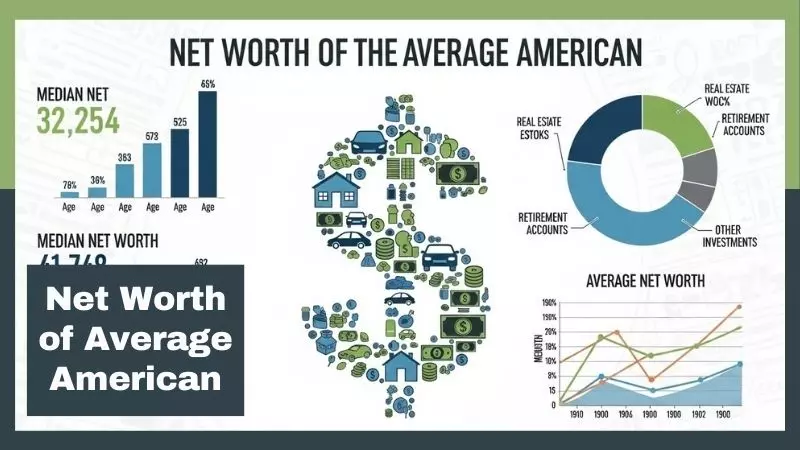

Average Net Worth vs Median Net Worth – Big Difference Explained

The difference between average and median net worth is often overlooked. The average can be skewed by ultra-wealthy individuals, while the median reflects the typical financial situation of most Americans.

Why it matters:

- Average net worth can appear high due to the top 1% wealth holders.

- Median net worth gives a clearer picture of middle-class financial health.

| Metric | Value (2026 Latest Data) | Insight |

| Average Net Worth | $432,000 | Includes high wealth outliers |

| Median Net Worth | $121,700 | Reflects the typical American household |

| Top 10% Net Worth | $1,200,000+ | Shows wealth concentration among the richest |

Understanding this distinction helps Americans set realistic financial goals and avoid misleading comparisons.

How U.S Total Net Worth Reached Trillions

The total net worth of U.S households has been growing steadily, reaching over $150 trillion in 2026. Several factors contribute to this:

- Rising property values have increased home equity for millions.

- Stock market growth has boosted investments in 401(k)s, IRAs, and other portfolios.

- Debt management improvements in some households.

However, it is important to note that wealth distribution remains unequal, with the top 10% owning a significant portion of the total net worth.

U.S Average Net Worth by Age – How Rich is Every Age Group?

Age plays a crucial role in wealth accumulation. Understanding average net worth by age helps Americans plan for retirement, investments, and debt repayment.

Net Worth by Age: 20s, 30s, 40s, 50s, 60s Breakdown

| Age Group | Average Net Worth | Key Notes |

| 20–29 | $14,000 | Early career, student loans, low assets |

| 30–39 | $91,000 | Growing income, paying mortgages, building retirement funds |

| 40–49 | $168,000 | Peak earning years, investing in homes and stocks |

| 50–59 | $250,000 | Higher savings, preparing for retirement, reducing debt |

| 60–69 | $400,000 | Retirement-focused, relying on pensions and investments |

Tips for younger Americans:

- Start retirement accounts early to benefit from compounding.

- Reduce high-interest debts before investing heavily.

Median Net Worth by Age – Where Do You Stand?

Median net worth often gives a more realistic financial picture than averages. Most Americans have much less than what the average suggests.

- Median net worth for 20s: $5,300

- Median net worth for 30s: $59,000

- Median net worth for 40s: $124,000

- Median net worth for 50s: $187,000

- Median net worth for 60s: $266,000

This highlights that half of Americans have less than these numbers, reinforcing the importance of budgeting and investment planning.

Top 10% Net Worth by Age – How Much Do the Rich Really Have?

The top 10% of Americans control a huge portion of wealth, showing how income inequality impacts net worth statistics.

| Age Group | Top 10% Net Worth | Key Insights |

| 20–29 | $140,000+ | Early investors and entrepreneurs |

| 30–39 | $650,000+ | High-income earners and early homebuyers |

| 40–49 | $1,200,000+ | Peak career earnings, diversified investments |

| 50–59 | $2,000,000+ | Strong retirement and investment portfolios |

| 60–69 | $3,500,000+ | Wealth accumulation before retirement, inheritances |

Actionable tips:

- Aim for investment diversification to grow net worth over time.

- Focus on long-term wealth accumulation instead of short-term spending.

- Learn from top earners: invest early, manage debt, and plan retirement.

Net Worth of a 30-Year-Old American – What’s Normal Today?

For many Americans in their 30s, understanding their net worth at age 30 is crucial for long-term financial planning. This period is often defined by career growth, home purchases, and starting families, which can significantly affect both assets and liabilities. Knowing what’s “normal” helps you benchmark your finances and adjust your saving and investing strategies.

Median Net Worth of 30-Year-Olds

The median net worth for Americans in their 30s is still modest compared to older age groups. Most are managing student loans, car payments, and early mortgages, which reduce the overall net worth.

| Metric | Value (2026 Latest Data) | Insight |

| Median Net Worth | $59,000 | Typical 30-year-old household net worth |

| Average Net Worth | $91,000 | Higher due to wealthier outliers |

| Top 10% Net Worth | $650,000+ | Early high earners, entrepreneurs, or investors |

Key takeaways:

- Focus on paying down debt to increase net worth faster.

- Invest in retirement accounts and stocks to build long-term wealth.

- Don’t compare yourself to averages; median numbers are more realistic for most 30-year-olds.

Financial Reality vs Expectations

Many 30-year-olds overestimate their wealth because income doesn’t always translate to net worth. Here’s a reality check:

- Reality: Many 30-year-olds have less than $60,000 in net worth, including debts.

- Expectation: People often assume they should have $100,000+ saved by this age.

- Solution: Build a budget plan, emergency savings, and investment strategy to gradually close this gap.

Understanding this gap is critical for making smarter financial decisions and planning for homeownership, retirement, or major life goals.

Net Worth of a 50-Year-Old American – Are You Ahead or Behind?

By age 50, Americans are usually in their peak earning years and have had decades to accumulate wealth. Comparing your net worth at 50 against national data helps identify whether you are on track for retirement readiness.

Average Net Worth at 50

| Metric | Value (2026 Latest Data) | Insight |

| Median Net Worth | $187,000 | Typical for a 50-year-old household |

| Average Net Worth | $250,000 | Skewed higher by wealthier households |

| Top 10% Net Worth | $2,000,000+ | Successful investors and high-income earners |

Tips for 50-year-olds:

- Focus on maximizing retirement contributions like 401(k)s and IRAs.

- Reduce debt aggressively, including mortgages or car loans.

- Evaluate investment diversification to protect accumulated wealth.

How Lifestyle & Savings Impact Net Worth

Lifestyle choices and saving habits have a significant impact on net worth by age 50:

- High spending with low savings can limit wealth accumulation even with a high income.

- Consistent investing over decades, even in small amounts, dramatically increases net worth.

- Homeownership and equity play a key role in building long-term wealth.

- Unexpected expenses such as medical bills can reduce net worth if no emergency fund is maintained.

Actionable advice:

- Track net worth regularly using financial planning tools.

- Set realistic goals for retirement, emergency savings, and debt repayment.

- Prioritize long-term investments over short-term spending to secure financial stability.

Household & Family Wealth in America

Understanding household and family net worth helps put personal finances into perspective. While individual net worth is important, family wealth reflects combined assets, debts, and financial stability. Many Americans underestimate the impact of shared liabilities like mortgages, student loans, and credit card debt on family wealth.

Average American Household Net Worth

Household net worth considers all assets owned collectively, including homes, retirement accounts, and investments, minus debts.

| Metric | Value (2026 Data) | Key Insight |

| Average Household Net Worth | $432,000 | Skewed by top-earning households |

| Median Household Net Worth | $121,700 | Represents typical family wealth |

| Top 10% Household Net Worth | $1,200,000+ | Wealthiest households hold most assets |

Key points:

- Home equity and retirement accounts are the largest contributors to household net worth.

- Families with multiple income sources usually have higher combined wealth.

- Tracking household net worth regularly helps in budgeting, investments, and retirement planning.

Average Family Net Worth – What Do Families Really Own?

Families often overestimate their net worth because debt reduces overall wealth. Realistic assessment includes:

- Real estate and property ownership

- Savings accounts and emergency funds

- Retirement accounts and investments

- Liabilities like mortgages, loans, and credit card debt

Understanding these numbers helps families plan for children’s education, home upgrades, and long-term savings goals.

Retirement Net Worth in America – How Much Do People Retire With?

Planning for retirement is closely linked to net worth accumulation. Knowing the average American net worth at retirement helps you measure if you are financially prepared for the future.

Net Worth of Average American at Retirement

| Retirement Age | Median Net Worth | Average Net Worth | Key Insight |

| 60–69 | $266,000 | $400,000 | Most Americans rely on Social Security and savings |

| 70–79 | $324,000 | $500,000 | Investment portfolios and pensions increase wealth |

| 80+ | $290,000 | $480,000 | Wealth may decrease due to medical and living expenses |

Important notes:

- Many Americans underestimate the amount needed for comfortable retirement.

- Early and consistent investing in retirement accounts significantly increases net worth.

- Tracking net worth helps avoid financial shortfalls during retirement years.

Net Worth of American Retirees – Are They Financially Safe?

Financial security in retirement depends on savings, investments, and lifestyle choices. Key factors affecting retiree net worth include:

- Health care costs which can reduce savings

- Inflation impacting purchasing power

- Social Security benefits supplementing retirement income

- Investment income from stocks, bonds, and real estate

Tips for retirees:

- Maintain a diversified portfolio to protect against market fluctuations.

- Reduce debt before retirement to maximize financial freedom.

- Regularly review spending and budgeting to stretch savings further.

Final Verdict – What Net Worth Should You Aim For?

Knowing your net worth target is essential for financial planning, wealth accumulation, and retirement readiness. Setting realistic benchmarks helps guide investments and spending decisions.

Wealth Benchmarks You Should Target

| Life Stage | Target Net Worth | Notes |

| 30s | $91,000+ | Focus on debt reduction and early investments |

| 40s | $168,000+ | Peak earning years, maximize retirement contributions |

| 50s | $250,000+ | Reduce liabilities, diversify investments |

| 60s | $400,000+ | Prepare for retirement and healthcare expenses |

| 70+ | $500,000+ | Maintain stable lifestyle, manage withdrawals carefully |

Key takeaway: Use these benchmarks as guidelines rather than strict rules. Personal situations vary, and long-term growth is more important than short-term comparisons.

How to Increase Your Net Worth Faster

Increasing net worth requires a mix of strategic saving, smart investing, and debt management.

- Track all assets and liabilities regularly to know your financial position.

- Maximize contributions to retirement accounts like 401(k)s and IRAs.

- Reduce high-interest debt, including credit cards and personal loans.

- Consider investing in stocks, real estate, or other long-term growth assets.

- Control lifestyle inflation, avoiding spending that exceeds income growth.

Focusing on these strategies consistently will help Americans grow wealth faster, achieve financial goals, and retire comfortably.

Frequently Asked Questions

What is the net worth of the average American in 2026?

The average American household net worth is around $432,000, while the median net worth is $121,700, reflecting typical financial health.

How much does the median American actually own?

Median net worth shows most Americans have about $121,700 in assets after debts, offering a realistic view of typical household wealth.

How does age affect the net worth of Americans?

Net worth increases with age; 20s average $14,000, 30s $91,000, 40s $168,000, 50s $250,000, and 60s $400,000 on average.

What is the top 10% net worth of Americans?

The top 10% of Americans have $1,200,000 or more, highlighting the wealth concentration among the richest households.

How does debt impact the average American’s net worth?

High debts, including mortgages and loans, significantly reduce net worth, especially for younger households with student loans.

What is the household net worth vs individual net worth?

Household net worth combines all assets and debts of family members, often showing higher values than individual net worth alone.

How much should an average American save to increase net worth?

Consistently saving 15–20% of income, investing in retirement accounts, and reducing debt can steadily increase net worth over time.

How does net worth differ across U.S states?

States with higher property values and incomes, like California and New York, show higher average net worth compared to lower-cost states.

Chriselle Lim is a passionate digital creator and lifestyle blogger based in California, USA. As the voice behind Blogzeno, she shares creative captions, inspiring Instagram bios, insightful celebrity stories, and simple insurance guides designed for everyday readers. Emily believes that words have the power to connect people whether it’s through a perfect caption or a helpful article.

With years of experience in online writing and content strategy, Emily’s mission is to make information both useful and enjoyable. Her work blends creativity with clarity, helping readers express themselves confidently and stay informed about what truly matters.

When she’s not writing, you’ll find her exploring photography, social media trends, and new ways to inspire digital creators worldwide. Follow her journey on Blogzeno — where creativity meets everyday life.